Economic development generally follows the pattern stated hereinafter. Initially, there is the ‘primary’ stage of an economy which comprises of activities that involve extraction, production and selling of raw materials.

Economic development generally follows the pattern stated hereinafter. Initially, there is the ‘primary’ stage of an economy which comprises of activities that involve extraction, production and selling of raw materials. As economic growth obtains momentum, the economy moves towards the next level, known as the ‘secondary’ stage. The secondary stage is built on industrialisation, saving, and producing, where more value has been added in the production. Moreover, as an economy continues its journey and transforms into an advanced stage, it moves from the secondary and to the ‘tertiary’ stage. The tertiary phase of an economy is where a country transforms from a developing to a developed economy. At the tertiary stage, the economic development brings with it a higher per capita income. This means that in the tertiary stage, people have higher purchasing power, a higher standard of living, and increased propensity to consume. The economy also increases its reliance on imports because they are cheaper than homemade goods.

However, not all economies follow this path necessarily. In particular, several countries may suffer from a premature ‘de-industrialisation’ stage where the share of commodity producing sector may begin to plunge without reaching its full potential.

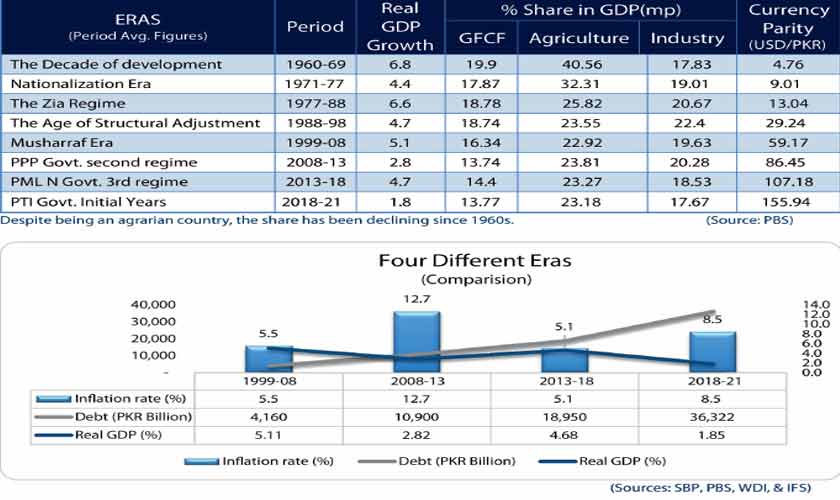

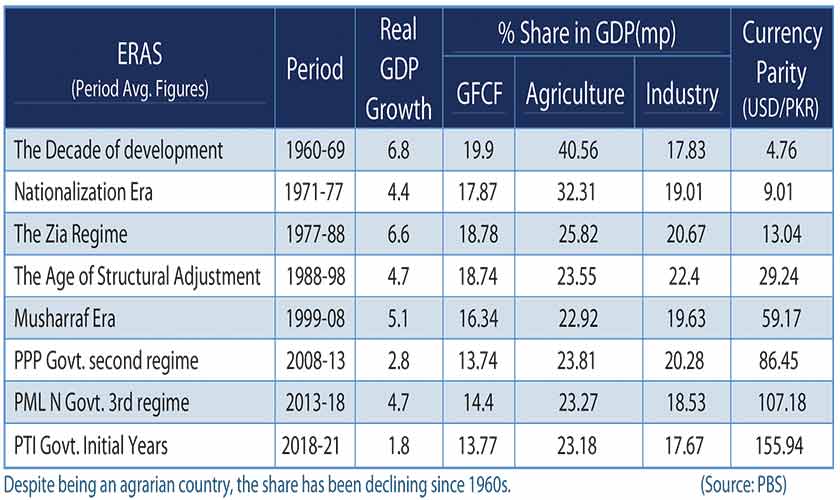

In 1947, Pakistan was, indeed, a preeminent agrarian, underdeveloped and a newly independent nation, with fewer industries, few services, and no substructure. It was the windfall profits made by the mercantile group during the Korean War in 1952 that eased the way to build a foundation. Between 1947- 1952, the average GDP growth of Pakistan GDP was 3 percent. However, when the aforesaid war broke out and the overall demand for commodities increased worldwide, Pakistan made the most of it with the GDP rising at a rate of 10.22 percent in 1953. That was the era during which we did not borrow a single penny. Later, there was a worldwide slump when the war had ended. Nonetheless, the Pakistani economy was rapidly revitalised under Ayub Khan’s era, and in hindsight, it has turned out to be the decade with the best performance as the average GDP growth stood at 6.8 percent. In this phase, one cannot underestimate the role of Pakistan Industrial Development Corporation (PIDC), which provided financial and technical assistance and set up those industries where most of the private sector was reluctant to invest. During this era, Pakistan progressed systematically towards industrialisation, and because of that the Pakistani economy moved from the primary stage to its secondary stage. However, soon after entering its secondary stage, the Pakistani economy received a rude shock in the shape of nationalisation. It is considered a rude shock because the economy of Pakistan took a vicious beating due to nationalisation, as our GDP growth decreased from 6.8 percent to 4.4 percent in that period, and simultaneously the role of the PIDC shrunk. At that time, huge investors, who were also known as the 22 rich families, who had thrived during the 60s, were brushed aside by the wave of nationalisation. The trust of these huge investors was shattered, and investment from all sectors started to decrease at an alarming pace. Due to this huge trust deficit, a massive outflow of capital was witnessed in Pakistan. If it was not for the nationalisation era, we might have continued the good trajectory our economy was headed towards, and therefore, we could also have had business magnates such as Jeff Bezos, the Ambanis, and the Mittals etc in Pakistan. Nationalisation had a huge contribution in stopping the Pakistani economy from entering into its tertiary stage in real terms.

Unfortunately, after that wave of nationalisation, we again transited towards the wrong direction due to an economic burst because of the Afghan war spill over. For Pakistan, war brought much harm to our society and politics, as Pakistan went through unsettling affects due to the war in Afghanistan, due to our close proximity to Afghanistan. Nevertheless, Pakistan is still, even four decades down the line, feeling the ferocious effects of the war in Afghanistan.

Pakistan’s democratic transition, after the death of General Zia in 1988, was matched by the introduction of a new economic chain, wherein, inter-alia, Pakistan joined the world of Structural Adjustment Programme(s). In 1992, Pakistan adopted the Protection of Economic Reforms Act (PERA), with an aim to facilitate financial liberalisation. However, PERA was misused by wrongdoers to amass wealth, and ended up creating a huge parallel economy base. The unfortunate bit is that the Pakistani economy is still suffering from the repercussions of the PERA due to the flourishing of the notorious ‘hawala and hundi’ business. Speaking of unfortunate tales, let me move on to another bad policy which was introduced in 1994. This policy was the policy for the Independent Power Producers (IPPs). Fair to say, that it has, at least in my humble view, transpired to be the worse economic decision that was opted for in the past three decades. The said policy included, private investors being allowed to build power generation projects (at very attractive rates) and any rise in the cost of fuels was to only be borne by consumers. Resultantly, Pakistan produced expensive power, which gave rise to circular debt and made Pakistan vulnerable to potential fuel crises.

Aside from the aforesaid blundersome IPP policy, let me candidly state one of the worst kept secrets of Pakistan, which is that it has been under the tutorship of multilateral lending institutions, such as the International Monetary Fund (IMF) and the World Bank. Henceforth, almost every decision, bearing any consequences taken by the several regimes that have been in power, was pre-ordained by these multilateral lending agencies, and Pakistan has merely followed their decree. During the 90s, despite having nominal growth, Pakistan failed to build a strong growth foundation. This had an adverse effect in the late 90s and early 2000s, particularly in the commodity producing sector.

It was only after the tragedy of 9/11 that the growth rates in industries, capital investment, and of the economy picked up, under Pakistan’s third autocratic government. The economic impact during the years following the tragedy of 9/11 was similar to the economic impact that the Afghanistan war had on Pakistan, to the extent that huge foreign aid facilitated Pakistan’s economy, after Pakistan declared its support to the USA as a non-NATO ally in the war in Iraq and Afghanistan. Furthermore, Pakistan witnessed a sudden rise in the frequency of terrorist attacks, when Pakistan began playing its role as a frontline country against terrorism. In the aftermath of these terrorist attacks, Pakistan incurred a cost to the tune of $126.79 billion (Annexure-IV, Economic survey 2017-18), indicating the economic impact of the war on terror faced by Pakistan, and that the growth rates, of the economy, investment, and manufacturing, dropped sharply.

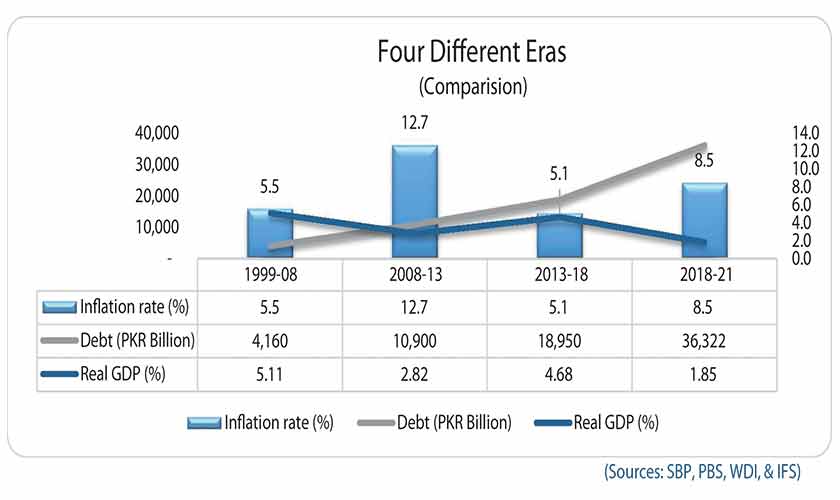

The boom of the Musharraf era was built upon the wrong foundations, which included largely consumer led growth and investments in stock market sectors, speculation with remittances, and as stated above foreign aid driving the growth. The missing link for then was a long-term strategy and route to guide this money being spent in to better (and) productive sectors. The Pakistan People’s Party (PPP), in 2008 acquired countless problems created by Musharraf and the caretaker governments, as the average GDP growth during 2008-12 was 2.81 percent, while the total debt and liabilities stood at a staggering at 66.6 percent of the GDP by the end of PPP’s democratic regime. Moreover, numerous external factors, such as the oil and food prices that rose, financial crisis in developed countries, the security concern(s) due to the war on terror, and damaging floods, all added to the difficulties of the aforesaid democratic regime.

One must wonder, as to what went wrong with the robust growth of the 1960s, nationalisation of the 1970s, structural adjustment of 1988, the 90s, 2000s and onwards. An unusual answer is that Pakistan’s efforts seem to be more tilted towards an ‘economic bonanza’, rather than ‘structural reforms’. Additionally, it may also be noted that Pakistan’s political economy is more dependent on external factors rather than internal factors. As a result, whenever Pakistan's economy reached the secondary level, we received windfall profits and we switched our economic priorities from ‘produce and sell’ to borrow and consume without achieving the full potential of our secondary stage, which translates into premature de-industrialisation, and hence real sectors (ie growth driving sectors) started to shrink. Under this premature de-industrialisation, our borrowing rises and it perishes the economic outlook of Pakistan.

The government has not done any work for stabilisation. Recently, they have been in talks to negotiate with the IMF, but the process has been really haphazard. Despite political stability and exceptional support from all the relevant quarters, the government will not lift the economy to a proper balanced growth path. Unfortunately, the economic policies are also based on the wrong premise, whereby, full potential is created in the secondary stage of our economy; however, the country jumps directly to the tertiary level.

Just recently, Pakistan had pursued a car financing scheme driven by a low borrowing cost and low down payment at 15 percent, which caused automobile financing to rise by 46.8 percent on year-on-year basis. Due to this policy, the automobile financing hit an all-time high of Rs326 billion in August 2021, which raised our import bill. However, the SBP subsequently jammed their brakes on the financing of imported vehicles, in order to slow down the deterioration in the trade and current account balance; albeit a bit too late, one can say.

Is it necessary for Pakistan to opt for such policies which is causing macroeconomic vulnerabilities such as a hike in inflation, the widening of the current account deficit, and the weakening of the currency parity? Similarly, taking into account the fact that the unstable situation in Afghanistan was likely to inflict more damage on the Pakistan economy, one wonders as to why this policy (car financing scheme) was introduced in the first place, and what particularly was the rationale behind it?

The economy could go back to the stop-go cycle. Moreover, the recipe of the economy for that should be the following: (i) The government must contain the secondary stage of their economy till five to ten years, until they fully capitalise on industrialisation and gradually move toward a balanced growth path, instead of endorsing any fancy policies; (ii) Keep the rate of interest rate low, because it will help the government to reduce debt-servicing in the short, medium and long-term. Low interest rates will also give a boost to businesses to operate on optimum level. Furthermore, a lower interest rate will also facilitate bringing down inflation given the fact of rising commodity prices; (iii) It is recommended to have a stable rate of currency parity which will facilitate the exporters in taking a long-term view of their businesses; and (iv) furthermore, it is also suggested that stringent exchange controls shall be imposed on luxurious imports and abnormal trading of foreign exchange. Besides that, the government will have to chalk on creating a long-term policy plan for import substitution through encouraging domestic production of raw materials and resolving grave issues in the economy to become self-sufficient which may help the country to improve its balance between international payments and receipts.

The writer is a senior tax consultant