Each year, millions of Pakistanis living abroad send their hard-earned money back home. In FY2022-23, Pakistan received over $27 billion in remittances, making it the sixth-largest recipient of remittances globally.

REMITTANCE PARADOX

Each year, millions of Pakistanis living abroad send their hard-earned money back home. In FY2022-23, Pakistan received over $27 billion in remittances, making it the sixth-largest recipient of remittances globally.

Remittances now account for over 8.0 per cent of Pakistan’s GDP, a figure that should place them at the heart of our economic strategy. Yet, despite this significant inflow, Pakistan has failed to convert remittances into sustainable economic development. In contrast, peer countries like Bangladesh, the Philippines, Egypt and India have used remittances as tools to support skill development, industrial upgrading and infrastructure investments.

This piece explores what Pakistan can learn from these countries and how we can reimagine our approach to remittances not just as a stopgap for foreign exchange crises, but as a strategic engine of national growth.

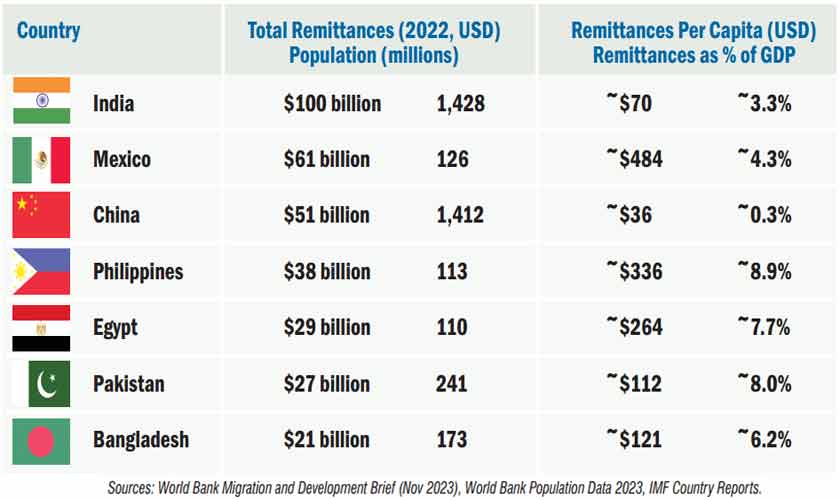

Let’s begin by examining how Pakistan compares to its peers in terms of remittance inflows. While Pakistan ranks high in total remittances, its performance is much weaker on a per capita basis. Countries like the Philippines and Mexico earn significantly more remittances per person and outperform Pakistan in utilising these funds through sound policy interventions. The Philippines, for example, earns $336 per capita in remittances, compared to Pakistan’s $112, and it also channels these inflows toward productive uses far more effectively.

In Pakistan, remittances are primarily spent on consumption -- covering daily expenses, buying real estate, or investing in non-productive assets. A State Bank of Pakistan study (2022) revealed that over 75 per cent of remittance-receiving households use the money for basic consumption. Only 6.0 per cent invest in businesses, and just 2.0 per cent direct funds toward education or skill development. In contrast, the Philippines has introduced government-sponsored programmes that funnel remittances into education and business ventures, making the flow more development-oriented.

The Philippines has long been a leader in managing remittances as a strategic resource. It established the Overseas Workers Welfare Administration (OWWA), which offers training and reintegration programs for returning workers. The country also launched investment platforms allowing overseas Filipino workers to invest in government bonds or business ventures back home. Skills certification programmes further enhance the labour quality of Filipinos working abroad, helping the country not only sustain remittance inflows but also improve its human capital.

Bangladesh, meanwhile, made remittance transfer easier and cheaper through mobile banking services like bKash. The government incentivized formal channels by offering a 2.0 per cent cash bonus on remittances sent through official means. Moreover, these funds are increasingly tied to micro, small, and medium enterprise development through subsidised loans, ensuring that remittances support grassroots-level economic activity.

India took a different approach by creating long-term investment opportunities for its diaspora, including India Development Bonds and Resurgent India Bonds. These instruments have been used to finance infrastructure projects, while also giving Non-Resident Indians a way to invest in their home country. In states like Kerala, specific policies have been introduced to support the welfare and reintegration of returnee migrants, creating a more inclusive and productive system.

Egypt has also been successful in leveraging remittances by offering real estate and investment incentives to the diaspora. Remittance senders enjoy preferential terms when purchasing land and property, and large contributors are offered dual citizenship benefits. These measures have helped Egypt maintain one of the highest remittance-to-GDP ratios while attracting funds into productive sectors.

In contrast, Pakistan’s remittance policy remains largely reactive. When foreign exchange reserves dip, authorities roll out short-term incentives like Roshan Digital Accounts or Naya Pakistan Certificates offering tax-free returns. While helpful in the short run, these schemes don’t tackle the core issue: the absence of an institutional framework that integrates remittances into national development priorities. There’s no coherent strategy linking these funds to industrial policy or vocational education. Investment vehicles for the diaspora are limited and short-term, and banking penetration among remittance-receiving households -- particularly in rural areas -- remains alarmingly low, hampering the use of digital channels.

To catch up with its peers, Pakistan must adopt a multi-pronged strategy that sees remittances not just as a source of foreign exchange but as development capital. First, it should establish a dedicated Migrants Welfare Authority to facilitate returnee reintegration through certifications, job matching and targeted training programmes. These efforts could be further supported by incentivising skill development among the youth in remittance-receiving households.

Second, the government should launch new diaspora-focused investment products, such as Pakistan Development Bonds with flexible terms, tax benefits and options to fund infrastructure or education. It could also create diaspora equity funds, enabling safe investments in business ventures or public-private partnerships that support long-term growth.

Third, Pakistan must formalise and digitise remittance flows. Expanding digital payment infrastructure, especially through partnerships with telecom companies, could make it easier and cheaper to send money home. Introducing small incentives for using formal channels, as Bangladesh has done, would further improve transparency and economic impact.

Finally, robust monitoring and transparency mechanisms are essential. Publishing an annual Remittance Impact Report would help policymakers understand trends, regional distributions, and the outcomes of existing programmes. Collaboration with academic institutions and think tanks could further improve the evaluation and effectiveness of remittance-driven policies.

Pakistan stands at a critical juncture. With over nine million overseas citizens, the country has a unique opportunity to turn remittance inflows into a cornerstone of long-term economic development. The examples of the Philippines, India, Bangladesh, and Egypt show clearly that it’s not just the volume of remittances that matters—it’s how they are used.

For Pakistan, the path forward lies in shifting the narrative: from remittances as charity to remittances as capital. That requires bold policy thinking, innovative financial products, and a clear alignment with national development goals. Remittances have already done much for Pakistan. With the right framework, they can do even more.

Note: Data sources used include the World Bank, IMF, State Bank of Pakistan and various national remittance boards.

The writer is an investment banker based in Riyadh, Saudi Arabia, with eight years of experience across consulting, corporate finance, strategy and investments. You can connect with him on LinkedIn: https://www.linkedin.com/in/mustafafahim/