On numerous occasions, an expression has been doing rounds in the media that Pakistan might default on its international debt obligations. In addition to the above, it has also been said that the growing import bill and soaring inflation is the indicator that suggests that Pakistan may default.

On numerous occasions, an expression has been doing rounds in the media that Pakistan might default on its international debt obligations. In addition to the above, it has also been said that the growing import bill and soaring inflation is the indicator that suggests that Pakistan may default.

Although all these rumors intensified when the Credit Default Swap (CDS) rose significantly to 93 percent amidst rumors that Pakistan might not repay its $1 billion payment for a maturing international bond early next month. However, the current minister of Finance has denied all these rumors/allegations and has gone on record to state that Pakistan will be repaying the international bond investors on time. Following this assurance, the CDS percentage has declined to 71 percent.

The purpose of this article is to explain the reason(s), why Pakistan will not even be close to default. To support this, the author will try to analyze the (rhetorical) claim that Pakistan will default, putting key macroeconomic indicators at the heart of the author’s analysis.

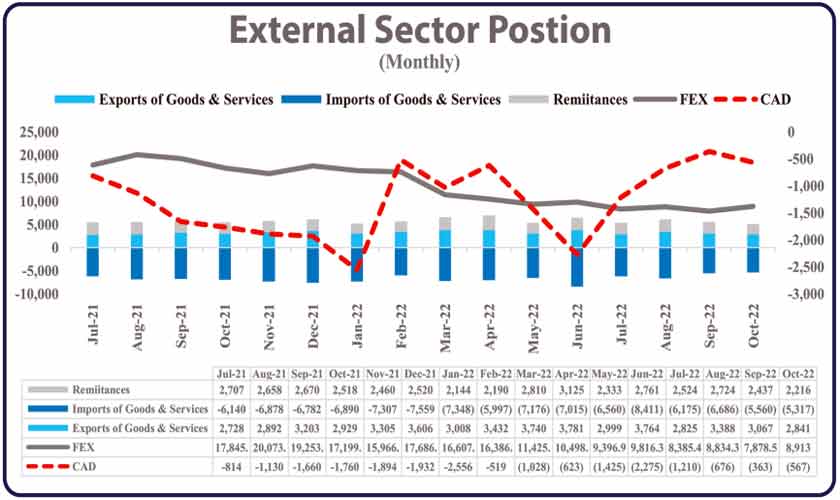

One may ask as to what the possible rationale is behind the recent rhetoric of economic default witnessed in the ongoing month. An analysis is undertaken to answer this very question. Whilst answering the said question answer, the author has compiled in the chart below the data of the foreign reserves and other important external sector indicators.

(See External Sector Position graph)

From the aforesaid chart, it is safe to say that the current regime is working proficiently to curtail the rising import bills by imposing a ban on import of unnecessary products. The impact thereof is quite visible in the recent trend of Current Account Deficit (CAD) figures released by the State Bank of Pakistan (SBP). In the previous fiscal year 2021-22, the CAD rose to an unprecedented level ($17.4 billion) and led to an uncertain behavior of crucial economic indicators such as rampant devaluation of rupee and a significant decline in foreign direct investment, henceforth, Pakistan had to implement a contractionary monetary policy.

In contrast, since the start of the ongoing fiscal year 2022-23 (FY23), the CAD is on a better and more sustainable level ($2.8 billion during the Jul-Oct period presently) as compared to the previous fiscal year where during the same period it stood at $5.4 billion. The drastic change in the CAD trend is clearly visible. In addition to this, since March 2022, the global commodity market chaos has begun amidst the Russian-Ukraine conflict and this has made the situation even worse.

At a time, when Pakistan faced such unforeseen events, the revival of the International Monetary Fund’s programme was a huge task for the government. The said IMF programme was stalled due to the deviation from commitments in policies by the previous regime. Owing to the above facts, Pakistan’s economic outlook in the last quarter of the previous fiscal year seemed to be trapped in a vicious cycle. The sharp rise in financing gaps in the government’s budget, as well as soaring debt and inflation, had pushed the economy towards a vulnerable position.

The floods destroyed huge masses of cultivated area and livestock in the country, creating a massive food supply disruption and therefore rendering Pakistan in a state of food insecurity. In this difficult period, Pakistan’s inflation rate surged to a record level, as the average inflation rate during the first four months of the ongoing FY23 was 25.5 percent. uring this challenging situation, the government did a great job to keep the average CAD below $1 billion during the Jul-Oct period.

Moreover, foreign exchange reserves depleted rapidly, and with that, pressure mounted on the Pakistani rupee, and this eroded business confidence. At that very moment when the above consequences arising due to the Pakistani economy living beyond its means were witnessed, it was perceived that Pakistan was moving towards a position whereby it may not be able to honor its external payment liabilities. However, things turned around when the new finance team got rid of the few economic dilemmas, and I must say that we ended up in a better and more positive direction. As a result of good administrative measures, the current regime was also able to control rampant devaluation of the domestic currency.

However, an unfortunate event occurred in July 2022 when Pakistan was hit by massive floods in most of the country’s rural areas. The floods destroyed huge masses of cultivated area and livestock in the country, creating a massive food supply disruption and therefore rendering Pakistan in a state of food insecurity. In this difficult period, Pakistan’s inflation rate surged to a record level, as the average inflation rate during the first four months of the ongoing FY23 was 25.5 percent. During this challenging situation, the government did a great job to keep the average CAD below $1 billion during the Jul-Oct period.

In the author’s opinion, this is an extremely appreciable approach as a surging CAD may create fluctuation in parity as a result inflation might go above 30 percent.

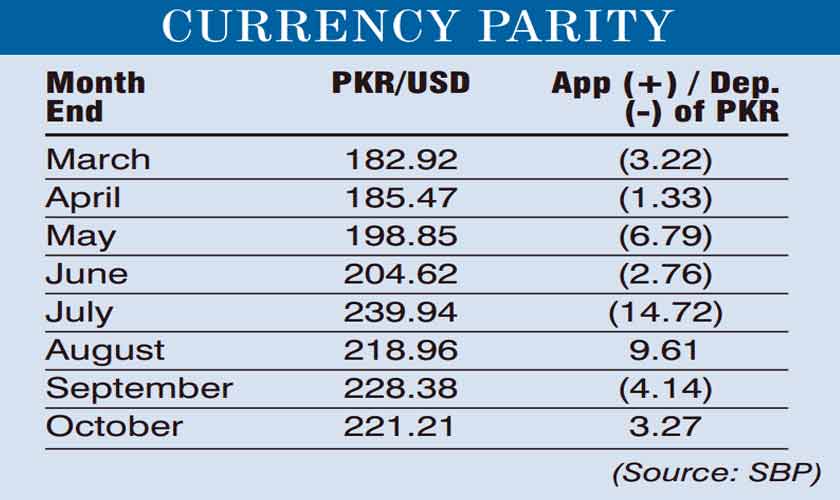

The table infra illustrates the parity trend since March 2022:

(See Currency Parity chart)

Even after a much better situation, we can still say that SBP’s held reserves have depleted rapidly to a very low level and it wouldn’t have happened if Pakistan’s economy had sustainable economic indicators back in FY22. As seen from the statistics published by the Pakistan Bureau of Statistics, Pakistan’s GDP grew by 5.97 percent in FY22, however the said growth might not be good enough as most of the macroeconomic indicators worsened and deviated from their targeted figures. The economic growth was mostly fueled with imports, as a result Pakistan faced a huge external sector imbalance.

Consequently, Pakistan had to face fiscal imbalances. In an interview given by the author back in August 2021, the author stated that CAD might rise to $16 billion with the policies of the previous regime. If the CAD had been controlled at that time or even set at its targeted level which had been predicted by SBP of $8 billion for FY22, then we might have had $9.4 billion more in reserves, and therefore we would have had a much stable picture of Pakistan’s economy. Although, due to unnecessary imports, we ended up with a huge external sector crisis. Despite all these economic fragile circumstances, the ongoing regime has done a fantastic job in controlling unnecessary imports which helped in reducing parity fluctuation and a controllable CAD, and leaving the interest rate unchanged in the ongoing FY23.

However, such measures to curb rising imports adversely affected our tax collection targets for FY23. At the end of the ongoing fiscal year we might face problems in achieving the tax target of Rs7.47 trillion , and the government will be very lucky if they attain the target agreed with the IMF.

Ultimately, as per economic indicators, we will not even be close to default and unfortunately such news is only circulating for political purposes. We must show some responsible behavior to support Pakistan’s economy in this rough patch. Although, it is common knowledge that today the economy of Pakistan is going through some of its crucial and difficult times, as we are with low foreign reserves and limited external sources of finance. Furthermore, the floods have raised more concerns.

The nation hopes that our finance team will take appropriate measures to stimulate our economy, and put the trajectory of Pakistan’s economy back on track and on a more sustainable level. The author prays that the nation once again rises from the multiple economic crisis that the economy is currently facing, and becomes stronger than before.

– The writer is a senior tax consultant