The Ministry of Information Technology and Telecommunication (MoITT) has issued a draft National Broadband Policy 2021 for consultation. The past policies, coming out of the ministry, were of high quality and praised internationally especially the Deregulation Policy 2003, Mobile Cellular Policy 2004 and Universal Service Fund Policy 2006.

The Ministry of Information Technology and Telecommunication (MoITT) has issued a draft National Broadband Policy 2021 for consultation. The past policies, coming out of the ministry, were of high quality and praised internationally especially the Deregulation Policy 2003, Mobile Cellular Policy 2004 and Universal Service Fund Policy 2006.

The Telecommunication Policy of 2015, though shied away from addressing most of the industry issues, it did pave the way for rapid uptake of mobile broadband by addressing the supply side. In this background, it was genuinely expected that the new sector policy will match the quality of previous policies and address the long pending issues of ICT sector, adjust the market structure and generate demand of broadband.

Government being the biggest consumer of any service, was also expected to step forward and create demand. This sector needs some serious attention from policymakers, as it is giving billions of rupees annually in taxes and levies, creating more than 450,000 direct and indirect jobs, coughing up billions of dollars in spectrum auctions periodically, laying down much needed digital infrastructure, contributing as much as 5.4 percent of the GDP and keeping the economy going during pandemic lock downs.

The purpose of any sector policy is to provide an enabling environment either by giving incentives and/or removing hurdles. Unfortunately none of this exists in the draft National Broadband Policy 2021. From plain reading of all 137 pages, it lacks substance and appears to be a very confused document with lots of repetitions from older policies and existing laws and regulations. There is absolutely no assessment, how much the previous policies were successful and what are the areas requiring corrections. Majority of stated policy statements/actions require either a study, formation of a committee or an action by PTA.

So the inference is that there was no market study, no gap analysis or data gone into developing this draft policy document. The draft policy creates too many unnecessary committees like service affordability committee, program review committees, management committee, tax reforms committee, steering committee, spectrum reframing committee, service affordability committee and multiple working group to do things, which should have been done in the policy itself. It would be wise to rename the document as committees’ policy rather than a broadband policy.

The industry has many big and small challenges inhibiting its potential to grow and serve the customers. Some issues requiring urgent attention, are: market structure, market failures, licensing, new spectrum, too many taxes and levies, digital infrastructure, number of SIMs, broadband, style of regulations, implementation of IPV6, etc. None of these have been addressed in the draft policy.

First and the foremost matter requiring attention of the policy maker is the market structure. The current structure was created through Deregulation Policy 2003 with vertical and horizontal separations. Mobile cellular market was separated from local loop (LL) and wireless local loop (WLL) markets, LL market from long distance and international (LDI) market and later LDI market was further sliced into infrastructure and tower markets. Class value added services (CVAS) was created as a separate sub-category for licensing. On top of all this, there are integrated licensees like PTCL, NTC and SCO.

After almost 18 years of deregulation, policy draft needs to critically review this structure and see if it is working or not. Clearly the WLL market is not doing well, foreign investors have pulled out, limited mobility restriction is taking its toll, and introduction of mobile broadband proved to be the final nail in the coffin.

They are holding valuable spectrum, which could have been better utilised by the mobile operators. Draft policy either needs to end WLL market by giving them compensation for surrendering the spectrum or give them full mobility. Even in the LL category, except two or three regional players, there is no success story. Similarly the international incoming market, with diminished access promotion regime, rock bottom international termination rate and storm of OTT players, is struggling to survive. These licensees had to form a cartel in the shape of International Clearing House (ICH) to survive, which was rightly declared illegal by the Competition Commission.

The business of tower and infrastructure companies is also not taking off, as none of the mobile operator has divested its towers so far and the tower companies are only working in the space of built-to-suit towers and managed services, which is not sustainable in the long run. Should the mobile operators be continued to allow to have multiple towers in same area or force them to share. Party autonomy and commercial deals are clearly not working here.

Geographically, coverage is no more an advantage for any operator in major cities and towns, so why there is need of replication of towers. Policy intervention to make tower licensee business viable is also an area of consideration. Even in the mobile cellular market, two operators are either dead or merged and one more operator is on that path.

The reason may be tough competition, intense price war, lack of needed spectrum or investment but the result would be reduced competition and less choice for the customers. This is again a policy question to be asked; is the reduced customer choice acceptable and what should be the right number of mobile operators for Pakistani market. The draft policy is silent on this.

Draft policy 2021 needs to re-look at the licensing framework and decide whether to continue with this fragmented licensing or move to unified licensing or service neutrality. Is it wise to have multiple categories of licenses for essentially providing similar services? Should the LL operators continue to have no roll-out and minimum quality of service (QoS) obligations? Should the limited mobility on data continue in WLL category? Shall the draft Policy continue to allow open licensing for LL, LDI, tower, infrastructure or figure out the optimal number in the face of potential market failure? How many and what kind of telecom operators are needed in the Pakistani market.

The vital questions is, should the policymaker continue to wait for market failure to happen or intervene and correct the structures to avoid it. The job of policy maker and regulator is not only to keep the competition going but also to foresee and prevent market failures.

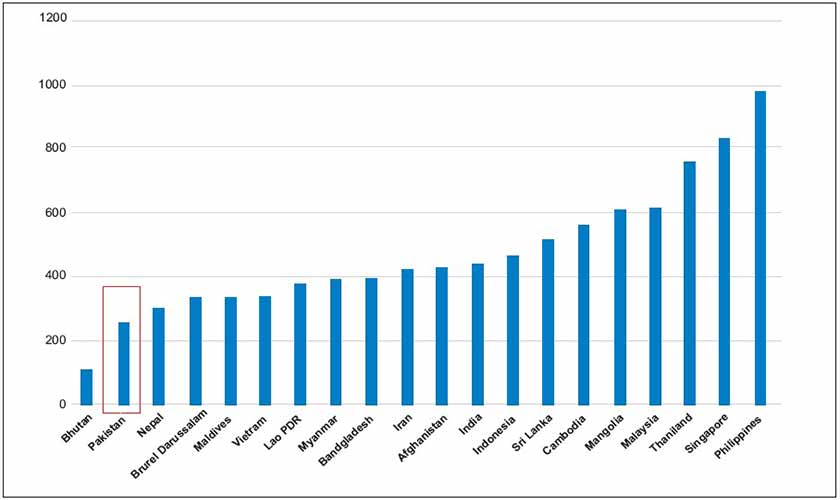

Next issue is spectrum, and its pricing. There is nothing new in the draft policy from that of Telecommunication Policy 2015.

According to the chart, IMT spectrum holdings is the second lowest in the Asian markets despite having the third largest population in the selected countries. Draft 2021 Broadband policy talks about administrative incentive pricing (AIP) and administrative cost recovery (ACR) for spectrum pricing. In the absence of adequate fiberisation of towers, AIP does not make sense as there is no alternative available, therefore AIP should not be put in practice till at least 60 percent of the towers are connected with fibre.

Even in the case of ACR, we need to keep in mind that 70 percent of the budget of FAB is borne by the mobile operators, which should be discounted from ACR calculation as 70 percent of the administrative cost is already paid by the mobile operators. Another important policy question under draft Broadband Policy 2021 is what kind of regulatory strategy, PTA needs to adopt after 17 years of deregulation. Should it be command and control or leave everything to the market forces for self-regulation or adopt a co-regulation style together with the industry.

The telecom sector is heavily taxed at all levels and in some cases even more than luxury items. This is possibly the biggest barrier to the growth and investment in the sector. In addition to sector specific taxes and tax rates, there are levies like contribution to USF, ICT R&D Fund, FAB and PTA. It is encouraging that the present government is reviewing the situation and certain decisions have been made in principle, however implementation of those decisions is yet to be seen. Interestingly, this issue has not been touched in the draft policy. Universal Service and ICT R&D Funds were created in 2006 with the aim of increasing telecom coverage and innovation in the ICT sector.

After 15 years of their existence, there needs to be a performance audit of both of these funds to see how much they have delivered on their mandate and what should be their role going forward. Do both the funds with their current spending trends, need the 1.5 percent and 0.5 percent contributions from operators, when a large sum from already contributed money, is lying idle in the Federal Consolidation Fund for many year.

Draft policy should recommend suspension of the obligation to contribute towards these funds for at least the next five years or till the already contributed money is exhausted. Similarly, the cost of regulation paid by operators towards PTA and FAB also need to be re-looked and rationalised. Surrendering excess budget to federal consolidation fund year after year is sufficient proof that PTA is extracting from the sector, more than what it needs to regulate. Mapping of available digital infrastructure is a must and a need assessment, as to what kind of infrastructure is required going forward.

Pakistan has graduated from 2G to 4G and planning to introduce 5G without addressing the back-haul. Even today the optic fibres only cover less than 10 percent of the total towers. So far the policy focus remained on access or last mile but now it should be back to back-haul in shape of a national fibre policy, or plan. So far half-hearted efforts have been made on moving to IPV6 from IPV4, it is time to make it mandatory in the draft policy.

Back in 2004, mobile number portability was considered a tool for promoting competition; however, it never even crossed two percent of total SIMs during its peak. With shift to data, the draft policy needs to re-look at the utility of number portability and if it is decided to be still useful and relevant then why not introduce it in the LL market too, where a phone number at a fixed location is clearly more important than in the mobile environment.

The number of SIMs per person was restricted by superior courts because of the then law and order situation which has improved significantly, therefore there is no need to continue with this restriction. With strong KYC like biometric verification and potential Internet of Things (IoT) boom in 5G environment, having such restriction would be counterproductive. Draft Policy has failed to address or end this restriction.

The draft Broadband Policy has not even tried to improve the definition of broadband despite the fact that mobile broadband was introduced in 2014 and the customers’ appetite for speed has increased manifold.

This is another potential area requiring rethinking, as to why put the definition of broadband in the license document and lose the ability to improve it for 15 years. This needs to be taken out of licenses and mentioned in the regulations so that improvement can be made on periodical basis. This should be applicable on all consumer protection matters.

There needs to be an analysis in the draft policy as to what should be in the licenses and what in the laws and regulations.

Back in 2003, laws and regulations were not fully developed, therefore everything was incorporated in the license, now the situation is very different. Quality of service (QoS) is an important subject from license obligation and consumer protection perspective.

Recent surveys show that people are not getting even a decent QoS on both voice and data. From operators’ point of view main reasons of compromised QoS are intense price war, insufficient spectrum, lack of fiberisation and government’s greed to maximise rent seeking (spectrum pricing, levies, taxes and renewal fees), leaving the sector with lesser resources to invest on QoS and modern services. These factors need to be addressed one way or the other in the draft policy.

Another point to debate is whether PTA really does need to be involved in Interconnection and termination rates, when the market is fully competitive. A non-discriminatory rule can efficiently run this market without need of any intervention unless there is fear of market failure.

There also needs to be a determination, if the termination rate at the current level is fair or is it a barrier to effective competition as the rate of off-net call is prohibitively expensive. There are lessons to be learnt from neighbouring countries in this regard. The draft policy has not even touched this important competition issue. Net neutrality is a much bigger subject than just writing few lines on Open Internet Rules in the draft Policy.

The biggest hurdle on open internet is government itself, with network shutdowns and blocking of content, websites and apps. In the 5G environment, net neutrality will become even a bigger issue as network slicing is an important feature and we cannot simply block that functionality without really understanding the technology and its potential use.

5G use cases range from ultra-reliable low latency communication like remote surgery and autonomous vehicles to latency tolerant communication like social media and video streaming. The draft policy under review also contains stuff, which is relevant for other industries and not for the ICT sector only.

Ease of doing business is an important subject and Pakistan needs to improve significantly to attract more investment in all sectors. Similarly, environment protection cuts across many industries and not just ICT. Fair use policy is not really a national policy level issue and should be left to PTA and operators with an aim to make the customers aware.

Regulating competition in all sectors is the mandate of Competition Commission including ICT. Through this draft broadband policy it cannot be taken from the Competition Commission and handed over to the PTA. It would be better to have a cooperation agreement between the two bodies to investigate unfair practices and take corrective actions.

Any different approach will require change in the Competition Law. In the absence of evidence, it appears that the targets set in the draft policy are not realistic and there is no mechanism prescribed for taking steps for achieving those targets and monitoring of their progress.

It is also interesting to note that there are so many resource-hungry action points but no funds have been allocated for meeting the cost of implementation of the draft broadband policy. Following statement towards end of the draft policy document clearly proves that it is not really a policy document: “It shall also help to do research where policy measures are required to uplift the telecom industry and to identify the bottle necks and show stoppers areas and where high efficiency can be introduced.”

The writer is an ICT regulatory expert