The first review of the $7 billion Extended Fund Facility (EFF) by the IMF is ongoing, making this a fitting moment to assess the macroeconomic landscape of the country.

The first review of the $7 billion Extended Fund Facility (EFF) by the IMF is ongoing, making this a fitting moment to assess the macroeconomic landscape of the country.

Headline inflation stood at 1.5 per cent year-on-year in February 2025, the lowest since September 2015. This decline is largely due to the SBP’s hawkish policy rate, a high base effect, favourable supply-side conditions, and the outdated weights of items in the consumer basket per Household Integrated Income and Consumption Survey (HIICS) conducted in 2015-16. However, this figure presents an illusion of stability; as they say, the devil is in the details.

Amidst the ‘economic revival’, unemployment has surged to 22.1 per cent as per the 2023 Census, compared to 6.3 per cent in 2021. Approximately 93 per cent of private-sector employees have not received wage increments, leading to a significant decline in real wages of almost 20 per cent over the last three years, first due to the Covid-19 crisis and later because of sluggish economic growth.

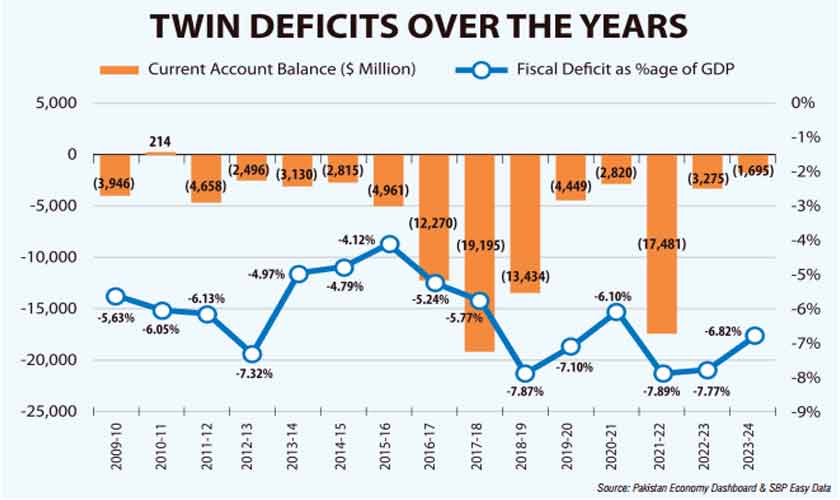

The macroeconomic picture is overshadowed by persistent twin deficits. Despite much-vaunted stabilisation, the trade deficit widened by 6.33 per cent in the first eight months (July-February) of the current fiscal year compared to the same period last year. On a year-on-year basis, February 2025 saw a sharp increase of 33.43 per cent in the trade deficit.

Exports for the first eight months stood at $15.78 billion, while imports reached $37.802 billion, leading to a trade deficit of $22.022 billion. These figures underscore the government’s myopia toward industrial reforms and hyperfocus on asset bubbles like real estate, highlighting the failure to revamp industrial policy, enhance export diversification, and curb non-essential imports.

Large-scale manufacturing (LSM) growth continued its downward trajectory, with December 2024 figures showing a 3.7 per cent year-on-year decline, bringing the cumulative growth for the first half of FY25 to a negative 1.87 per cent -- the lowest in 14 months. Further, the power sector remains in turmoil, with circular debt soaring to nearly Rs2.4 trillion by the end of FY24, adding Rs140 billion in two years. Weak demand due to rising tariffs, the increasing shift to solar energy, and inefficiencies in distribution and transmission have left the sector on the brink of collapse. This crisis not only cripples the export sector but also deepens poverty by eating household incomes.

On the fiscal front, the situation is dire, as revenue collection has failed to show substantial post-inflation growth since 2008, despite successive increases in tax rates across income and sales tax regimes. The FBR is already lagging behind its target by Rs606 billion in the first eight months of the fiscal year. The narrow tax base -- only 13.5 million filers compared to the 66.2 million employed -- combined with weak enforcement and an inefficient revenue collection system, exacerbates the shortfall.

The circumvention of taxes by retailers, urban real-estate players, and agriculture supply chain actors continues unchecked. The failure of the Tajir Dost scheme exemplifies the challenges of broadening the tax net, while the high reliance on indirect taxes (which have consistently accounted for around 80 per cent of total tax collection over the past five years) further burdens the lower-income population.

The much-touted rightsizing initiative remains largely cosmetic. The state-owned enterprises (SOEs) continue to drain public resources, with aggregate losses of Rs851 billion in 2023-24 and total loans reaching Rs9.2 trillion -- nearly equal to FBR revenues -- posing serious financial and credit risks. Over the past decade, cumulative SOE losses have amounted to Rs5.595 trillion. Adding fuel to the fire, the federal cabinet was recently doubled, bringing the total size of the body to 51 members, with obvious HR costs to be uplifted by the frayed shoulders of good taxpayers.

SOE reforms, especially in the power sector, are imperative. Privatisation and performance-based accountability must be introduced to halt financial haemorrhaging. Meanwhile, circular debt accumulation must be addressed through tariff rationalisation, improved efficiency in the supply chain and renewable energy integration

Meanwhile, the salaried class continues to bear a disproportionate tax burden. Income tax payments from salaried individuals surged by Rs103 billion in the first seven months (July 2024 to January 2025), reaching Rs368 billion -- far exceeding government projections. Tax contributions from corporate sector employees increased by 50 per cent, while provincial and federal government employees paid 96 per cent and 63 per cent more, respectively, compared to the previous year. Overall, revenue from this group grew by about 40 per cent year-on-year, highlighting the unequal distribution of the tax burden.

Debt indicators paint an equally bleak picture. The government allocated Rs7.5 trillion for debt servicing in FY24, but actual expenses exceeded Rs8.2 trillion, severely constraining development and social spending. And now the government debt surged by Rs2.73 trillion (4.0 per cent) in the first six months of FY25, reaching Rs71.6 trillion, while payments stood at Rs5.1 trillion (45 per cent of total expenditure). If this trajectory continues, interest payments will exceed Rs10 trillion in the remaining six months, surpassing the budgeted Rs9.7 trillion. This unsustainable path limits fiscal space for education, health and climate resilience, ensuring that progress remains stalled.

All this imprudent at best and reckless at worst economic wizardry fuels the engine of dismal human development. Pakistan’s Human Capital Index (HCI) score, at 41 out of 100 according to the World Bank’s Country Partnership Framework, remains dismally low for its income level. This has resulted in rising poverty, with 45.5 per cent of the population -- around 110 million people -- living below the poverty line, marking an increase of 31 million in the past four years, as highlighted by Hafiz Pasha.

The widely celebrated NCPI figures fail to reflect the true economic reality, as even the IMF has revised Pakistan’s growth forecast downward from 3.2 per cent to 3.0 per cent. Addressing the twin deficits requires structural reforms rather than superficial fixes. These reforms must be indigenous, not externally dictated, as past multilateral loan-driven adjustment programs have largely failed to deliver sustainable improvements.

Pakistan’s trade policy needs a strategic reorientation toward resilience and long-term growth. This means moving away from overreliance on traditional markets and low-value exports while strengthening domestic manufacturing. Export diversification, investment in value-added industries and regional trade integration should be central to this shift.

Fiscal reforms must focus on expanding the tax base to include previously excluded sectors -- particularly real estate, retail and agriculture -- while curbing elite capture and wasteful expenditures. Over-reliance on indirect taxation must be reduced to ensure a more equitable tax system.

Development spending should prioritise human capital rather than infrastructure alone. Increased investment in education, healthcare, and climate resilience will yield higher long-term economic returns than politically driven, capital-intensive projects.

SOE reforms, especially in the power sector, are imperative. Privatisation and performance-based accountability must be introduced to halt financial haemorrhaging. Meanwhile, circular debt accumulation must be addressed through tariff rationalisation, improved efficiency in the supply chain and renewable energy integration.

A data-driven policy approach should replace reactive decision-making. Strengthening the Tax Policy Office (TPO), digitising the economy to curb informality, and enforcing compliance through technology-driven audits will be crucial steps toward fiscal discipline and economic stabilisation.

Only a bold, indigenous, and data-backed reform agenda can break the cycle of short-term fixes and put Pakistan on the path to sustainable growth.

The writer is a Peshawar-based researcher who works in the financial sector.