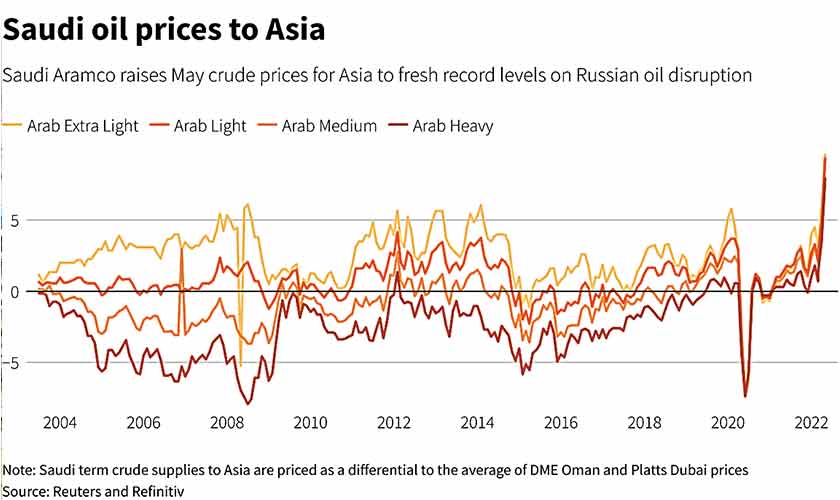

The jump in Saudi Arabia’s crude oil prices for its Asian customers is a real world example of how the Russian invasion of Ukraine is starting to force a realignment of global oil markets.

_magazine.jpg)

The jump in Saudi Arabia’s crude oil prices for its Asian customers is a real world example of how the Russian invasion of Ukraine is starting to force a realignment of global oil markets.

Saudi Aramco, the state-controlled producer, raised its official selling price (OSP) for its flagship Arab Light crude for Asian refiners to a record premium of $9.35 a barrel above the Oman/Dubai regional benchmark.

An increase in the OSP had been anticipated, with a Reuters survey of seven refiners estimating the price would rise to a premium of between $10.70 and $11.90.

This means the actual increase from April’s premium of $5.90 to May’s $9.35 was somewhat below market expectations, but still highlights that refiners in Asia are going to be paying considerably more for Middle East crudes.

Nevertheless, the $4.40 a barrel increase for May Arab Light crude price was slightly below the $5 hike expected in a Reuters survey. Saudi Aramco might have tempered the price hike after it raised prices more than expected in April.

Asia saw the biggest price increases across all crude grades, followed by Northwest Europe, the Mediterranean and the United States.

The record Saudi crude prices for Asia come as oil exports from Russia are hit by buyer aversion and western sanctions on the world’s top exporter of crude and oil products combined following the Ukraine conflict. Oil markets could lose 3 million barrels per day (bpd) of Russian crude and refined products from April, the International Energy Agency (IEA) said in March.

There are several factors at work driving the increase in Saudi OSPs, which tend to set the trend for price movements by other major Middle East exporters.

Spot premiums for Middle East grades hit all-time highs in March, a sign that usually points to higher OSPs as it signals strong demand from refiners.

However, these have slumped in recent trading sessions as physical traders mulled the impact of more crude being released from the strategic reserves of major importing nations, led by the U.S. commitment to supply 180 million barrels over a six-month period.

Another factor driving the increase in the OSPs for May cargoes is the strong margins being enjoyed by Asian refiners, especially for middle distillates, such as diesel.

Robust refinery profits are also usually a trigger for producers to raise crude prices, and currently a Singapore refinery processing Dubai crude is making a margin of about $18.45 a barrel, which is more than three times the 365-day moving average of $5.03.

But behind all these factors is the dislocation of global crude markets caused by Russia’s Feb. 24 invasion of neighbouring Ukraine.

While Russia’s crude oil and refined product exports have not been targeted by Western sanctions, buyers are starting to shun Russian cargoes and seek alternatives. Russia exported up to 5 million barrels per day (bpd) of crude and around 2 million bpd of products, mainly to Europe and Asia, prior to the conflict.

Russia’s crude and product exports are yet to show any meaningful decline, with commodity analysts Kpler putting March crude exports at 4.56 million bpd, down only a touch from 4.60 million bpd in February.

But the self-sanctioning of Russian crude is likely only to start being felt in April and May, as cargoes loaded in March would have been secured before the Feb. 24 invasion, which Moscow refers to as a special military operation.

Asian importers such as Japan and South Korea may start to pull back from buying Russian crude, meaning they will be keen to source similar grades from the Middle East, thereby likely boosting demand for cargoes from Saudi Arabia and other exporters such as the United Arab Emirates and Kuwait.

Conversely, China, the world’s biggest crude importer, and India, Asia’s second-biggest, may well try to buy more Russian cargoes, given both countries have refused to condemn Moscow’s attack on Ukraine.

India in particular will be keen to secure heavily discounted Russian cargoes, with some reports of Urals crude being offered at discounts of $35 a barrel or more to global benchmark Brent.

There are several key questions that remain to be answered, including how much more Russian crude can China and India actually buy, and arrange to transport, especially from the eastern ports that used to mainly ship to European refiners. The United States will not set any “red line” for India on its energy imports from Russia but does not want to see a “rapid acceleration” in purchases, a top U.S. official said last week during a visit to New Delhi.

It is also still unclear just how much self-sanctioning will cut Europe’s and Asia’s imports of Russian crude.

What is likely to happen is that Europe and the democracies in Asia, such as Japan and South Korea, effectively swap with China and India their Russian cargoes for Middle Eastern grades.

Even so, this is unlikely to soak up all the Russian crude that will be available, meaning the market will still have to find additional barrels, and Middle East exporters will be likely to continue to keep OSPs at elevated levels.