In my previous article that was published in February 2020, I had estimated the re-profiling of debts and fiscal deficits, and its consequences. Through the said article, I had suggested to reduce the policy rate to 7 percent and had further highlighted the adverse impact of hot money in the economy. However, the impact of hot money was realized later when the damage had already been done. Even though, the Pakistani economy has managed to recover recording a 3.94 percent provision GDP growth in the preceding fiscal year, it was asserted by some of the Pakistani economists that this provisional GDP growth has been recorded at the pertinent percentage due to a low base effect. Speaking of myself, I had asserted this GDP growth figure as ‘Flying with broken wings’ in my Firm’s annual publication ‘Overview of Pakistan Economy 2020-21’.

In my previous article that was published in February 2020, I had estimated the re-profiling of debts and fiscal deficits, and its consequences. Through the said article, I had suggested to reduce the policy rate to 7 percent and had further highlighted the adverse impact of hot money in the economy. However, the impact of hot money was realized later when the damage had already been done. Even though, the Pakistani economy has managed to recover recording a 3.94 percent provision GDP growth in the preceding fiscal year, it was asserted by some of the Pakistani economists that this provisional GDP growth has been recorded at the pertinent percentage due to a low base effect. Speaking of myself, I had asserted this GDP growth figure as ‘Flying with broken wings’ in my Firm’s annual publication ‘Overview of Pakistan Economy 2020-21’.

The current situation between the government of Pakistan and the International Monetary Fund (IMF) is that there has been a staff level agreement, and that the next meeting of the executive board of the IMF will be held in January to finalize the loan tranche. However, the IMF has prescribed certain measures as a prerequisite to obtaining the next available tranche that has been referred to supra, as per the IMF statement released on November 21, 2021. These measures seem tough, as the cumulative fiscal effect of these prior actions is around Rs800 billion, which includes a Rs250 billion cut in spending and Rs550 billion taxation measures during the remaining part of the ongoing fiscal year. It may be noted that Rs800 billion is equal to 1.5 percent of the gross domestic product (GDP) of Pakistan, making it one of the steepest adjustments in the midst of the recovery of our economy. Moreover, the tax collection target of the Federal Board of Revenue (FBR) has also been increased to Rs6.15 trillion, an addition of roughly Rs350 billion. These tough supplementary agreements will lead the economy of Pakistan into a havoc like situation, as the economy is already suffering from a hike in inflation and a poor external account position.

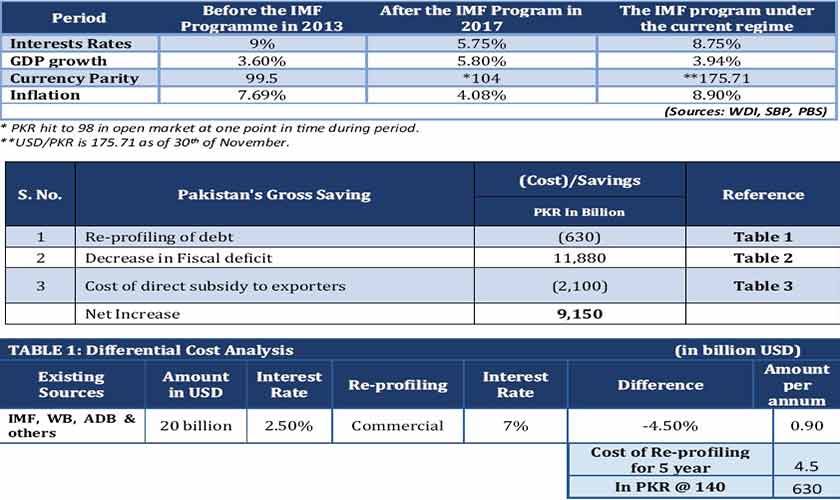

A point worth mentioning here is that despite the IMF's (tough) conditions in our past bailout programmes, the IMF programme under the previous regime was the only IMF programme in which Pakistan managed a good growth of 5.80 percent. During the same period, the inflation and interest rates remained at historic low levels, and our currency was stable as the rupee was valued at Rs104 against the US dollar. These factors had restored the investor’s confidence in Pakistan.

Despite positive indicators in the fiscal year 2017-18, Pakistan's economy has yet again slumped into a deteriorating position. The GDP is sliding down, and our economy is suffering on the back of, inter-alia, the domestic currency losing its value and alarming rise in debts. This raises questions as to why the current IMF programme has not been negotiated properly, why is it not being managed properly in terms of its implementation, and who is responsible for this failure?

As per news circulating in the media, the government officials have failed to negotiate with the IMF on major proposals for the amendments to the SBP Act 1956, which includes the request (from the government) to keep a door open for borrowing from the SBP. Similarly, the IMF has turned down the government proposal to take loans equal to 2 percent of the GDP in a fiscal year. So, to have agreement with the IMF, the government has now given up and agreed to permanently close this door through legislation. It is ensured that bailout programmes under the IMF ideally seek to bring fiscal discipline. Pursuant to the fiscal policies set out in the IMF programme(s), the finance ministry tends to avoid giving tax concessions and preferential treatments and works on plugging leakages to create fiscal resources to achieve the required objectives.

However, in case of an eventuality where there the government fails to reach an agreement with the IMF, the re-profiling of the economy of Pakistan is inevitable and may prove to be a blessing in disguise. I have done a cost-benefit analysis of the reprofiling of the economy. The cost-benefit analysis has been spelled out below.

Re-profiling of the economy

Pakistan can switch gears, going from a depleted growth to a high GDP growth, which may pave the way for Pakistan to live without the IMF in the long term, and come out of a vicious debt trap.

The economy of Pakistan, having a huge parallel base, does not have the capacity to follow the (harsh) prescriptions of the IMF. Instead of the IMF, we should move towards commercial borrowing and reduce the rate of interest to 4 percent. Moreover, the currency parity (rupee to dollar) should also be brought down to Rs140 to control inflation. Furthermore, there is a dire need to vigorously regulate the exchange regulations. Pakistan also needs to stay in the secondary stage of economy and realise its true capacity and potential therein, rather than jump to the tertiary stage of the economy. Additionally, the exporters should be heavily subsidized in rupee terms to ensure the exports remain competitive.

The updated financial impact of the following three factors on our economy would be Rs9,150 billion.

Pakistan is to receive $20 billion from the World Bank, Asian Development Bank, the IMF, and other bilateral/multilateral sources over the next five years. However, by incorporating the aforesaid loans, Pakistan will incur a negative Rs630 billion cost against the weighted average of the funding amount in the remaining five years.

Re-profiling of debt: With the re-profiling of debt, Pakistan's incremental cost would be around USD 0.90 billion per year, leading to an aggregate cost of PKR 630 billion at the USD to PKR Parity rate of PKR 140. The table infra contains the differential cost analysis of the reprofiling debt:

Pakistan is to receive USD 20 billion from the World Bank, Asian Development Bank, the IMF, and other bilateral/multilateral sources over the next five years. However, by incorporating the aforesaid loans,

Pakistan will incur a negative PKR 630 billion cost against the weighted average of the funding amount in the remaining five years.

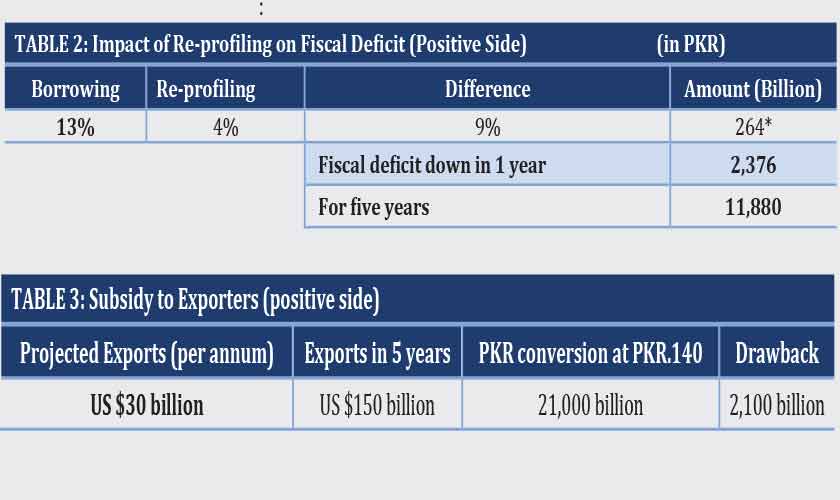

Re-profiling of the fiscal deficit:

With every percentage point increase or decrease in the interest rate, the fiscal deficit simultaneously increases or decreases by a net Rs264 billion. A reduction in the interest rates to 4 percent is suggested in order to accumulate projected savings of Rs11,880 billion over the next five years.

With a cut in interest rates, the industrial sector activity will revive, and inflation will slide, with demand expected to increase. Pakistan would, therefore, have more fiscal space with additional resources of Rs11,880 billion to push the GDP growth forward.

Subsidy to exporters: It is projected that an increase in Pakistan's exports up to $30 billion will come forth, when a direct or indirect cash subsidy of 10 percent of the total exports to the entire chain of exportable good and services. The value addition to the overall economy will also increase. The aforesaid benefit is linked with a currency parity of Rs140 to the USD and will help restore the competitiveness of Pakistan’s exports with the rest of the world.

Coupled with the aforesaid suggestions, the government must prioritize spending, rationalise expenditure, and shift towards development and quality of spending along with the cost benefit analysis of incremental spending. The government should also strictly adhere to pursue a fiscal management strategy, to honor the Fiscal Responsibility and Debt Limitation Act, 2017 to reduce public debt. Furthermore, tax reforms should be pursued, and the tax system must be made an equitable one for the betterment of Pakistan.

The writer is a senior tax consultant