Morgan Stanley Capital International (MSCI) will announce the re-classification of Pakistan to Frontier Markets Index (FM) on September 7, 2021, from the current classification of Emerging Markets Index (EM). The announcement will take effect in November 2021 and coincide with MSCI’s November 2021 Semi Annual Index Review.

Morgan Stanley Capital International (MSCI) will announce the re-classification of Pakistan to Frontier Markets Index (FM) on September 7, 2021, from the current classification of Emerging Markets Index (EM). The announcement will take effect in November 2021 and coincide with MSCI’s November 2021 Semi Annual Index Review.

The shift will likely bring positive inflows of investments in the short-run and provide impetus for more stable foreign portfolio investments inflows in the long-run, as is signaled by the FPI inflows and outflows from before and during the time Pakistan remained under EM index.

Immediately after Pakistan was classified to Emerging Index in 2017, foreign portfolio investment (FPI) inflows and outflows began to show results.

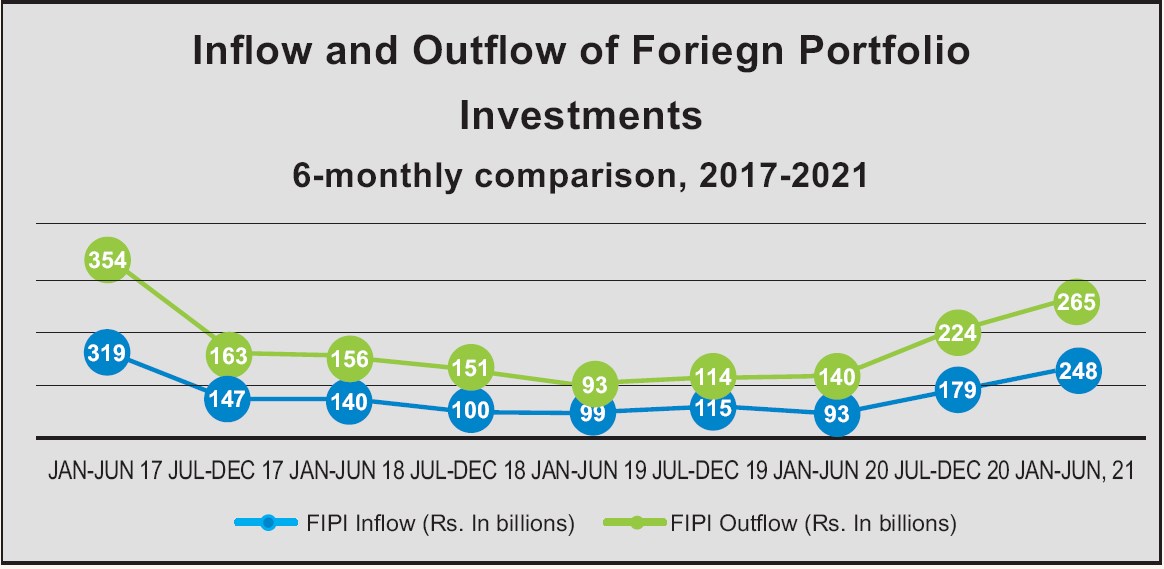

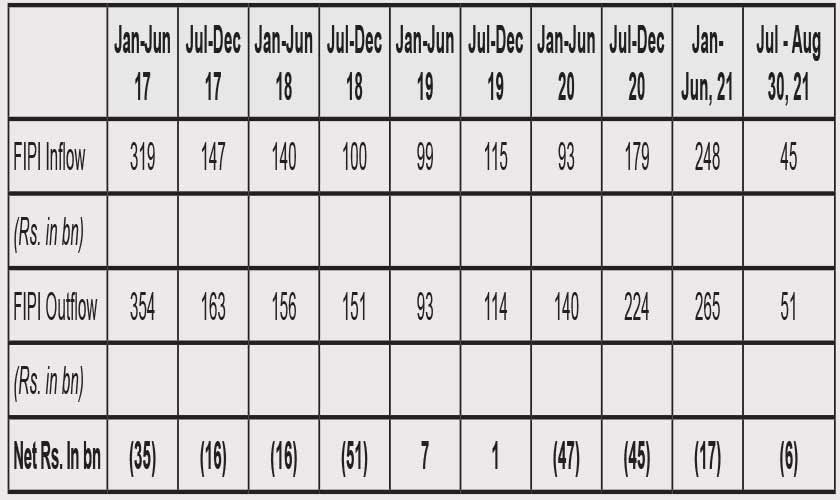

Data by the National Clearing Company of Pakistan Limited (NCCPL) shows how FPI started to fall steeply right after Pakistan’s transition to EM index. Within a year of announcement, the FPI had less than halved from Rs319 billion in June 2017 to only Rs140 billion by June 2018. This continued to decline until June 2019 when the recorded FPI was merely Rs99 billion.

This was an expected impact, as the MSCI classifications do not impact the investment decisions of veteran investors more than just acting as an explanatory tool. The lower weightage of the PSX in the index only meant that even the investors with higher risk appetite could now afford to ignore investments in Pakistan and retain a minor tracking error.

A shift was seen in Foreign Portfolio Investment in the first half of fiscal year 2020, to reach Rs248 billion by June 2021, as shown by the table. However, this change is not related to any development relevant to the MSCI classifications. In fact, that came as a result of the several initiatives undertaken to increase access to the Pakistani market and enhancing ease of doing business.

FPI picked up in 2020 on the back of the establishment of RDA framework for NRPs, relaxing documentation requirements for foreigners and online account opening facility.

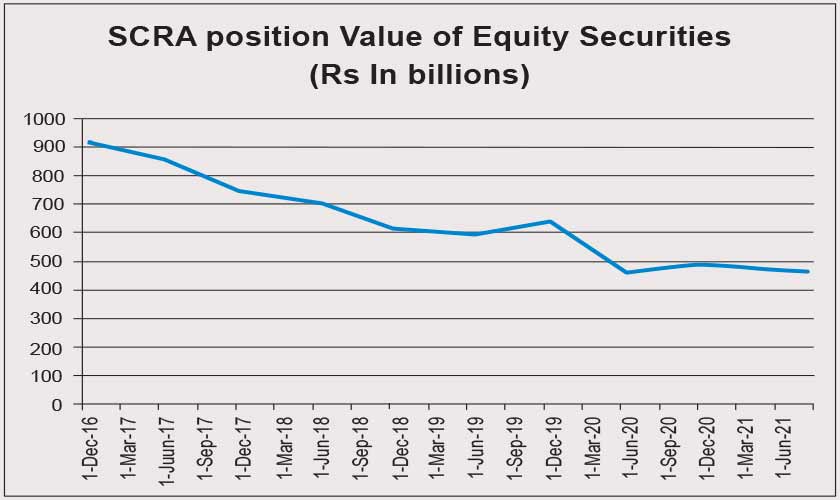

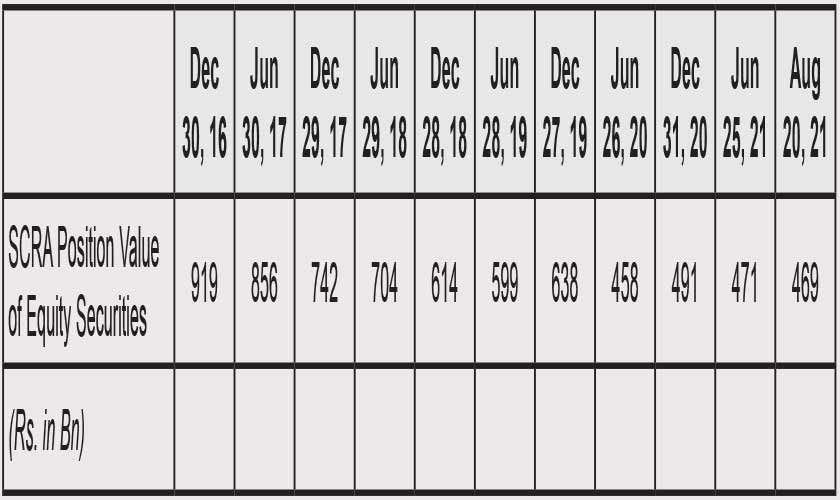

Backing this NCCPL data is the trend of Special Convertible Rupee Account (SCRA) position value of equity securities. This data is maintained by the State Bank of Pakistan (SBP).

SBP data also shows that foreign holdings under the SCRA since January 2017 showed a declining trend as well. It is worth noting that over 20 percent of the foreign capital in Pakistan eroded within a little over a year of transitioning to the emerging index, with a total decline by approximately 49 percent over four years till date.

Data of Pakistan Stock Exchange (PSX) tells a similar story, whereby a tangible impact was seen on the trading activities in the market. Turnover and traded value reduced significantly until recent recovery after June 2020, which again could be attributed to the central bank’s measures of allowing investment access to overseas Pakistanis, and not the fund managers tracking MSCI index.

So why did FPI decline so drastically after Pakistan’s transition into EMI?

MSCI is one of the various global index providers for fund managers to track. The two classifications under concern – FM may be understood as a basket of ‘high risk, high reward’ investments, and the EM classification as a category that lists ‘higher stability, lower risk’ stocks. Both classifications attract different types of investors, with varying risk appetites.

MSCI had listed six Pakistani companies under EM in June 2016. These were HBL, MCB, Lucky Cement, Engro, UBL, and OGDC. However, soon after in November 2017, Engro was removed, followed by UBL and Lucky Cement in November 2018. Even the remaining three companies are significantly below MSCI’s Full Market Cap and Free-Float Market Cap thresholds. The only reason they were still being retained was due to MSCI’s index continuity rules.

In June 2021, when the MSCI announced Pakistan’s reclassification, it noted that Pakistan’s stature in emerging markets had been artificially maintained since the country has been no longer meeting EM standards for size and liquidity criteria for the last 19 months.

This meant that even though the umbrella classification of MSCI had Pakistani companies among the potentially attractive investments for investors who prefer lower risk securities, the actual state of the stocks was nowhere close to fulfilling the metrics that such securities need to offer to attract foreign investment inflows.

Furthermore, MSCI index does not have any stronghold impact on investment decisions of veteran investors, thereby reducing the potential advantages of the classification even more.

Additionally, the low number of securities included from Pakistan also meant that overall weightage of Pakistani stocks in the index was persistently low at 0.02 percent according to a document on Consultation on a Market Reclassification Proposal for the MSCI Pakistan Index, MSCI June 2021. As a result, Pakistan was not able to utilise its classification under the EM index.

FPI inflows showed a marked decline during the time PSX was classified under the EM index. Experts opine that this is because with only a negligible weightage of Pakistan’s securities in the index, investors could afford to not invest in the Pakistani market and retain a minor tracking error.

However, during the time PSX was classified under the FM Index, from 2009 to 2017, 16 of Pakistan’s stocks were included as part of the index, attributing a 9.2 percent weightage to PSX. That meant that with this significant weightage, the fund managers tracking MSCI could not find it viable to ignore investing in Pakistan. The FPI were also significantly higher at the time, with $306 million in June to December 2009 and $530 million inflows in the following year.

This time around, Pakistan will have 2.3 percent weightage in the overall ‘FM index’, with a 5.8 percent weightage in the ‘FM 100’ Index.

This decline has come on the back of overall market cap decline for Pakistan’s securities as well as Pakistani rupee’s deterioration against the dollar.

This is also despite the fact that the FM index will have a much higher number of securities (19) from the PSX, as compared to only three under the EM index. The silver lining to this is that whatever the outflows of investments take place from the three securities under EM after the reclassification, the inflows from the securities under the FM are more than likely to offset them, experts said.

The writer is a freelance contributor