It is about time that the agenda of tax reforms was implemented in its true spirit. The positive outcome of doing this will be unlocking tax revenue potential and fixing tax revenue-gap, which is intrinsic for Pakistan’s economic sustainability. Moreover, this can also help augment sustained public finances, broaden the tax base and accelerate GDP growth. Developing countries like Pakistan should have growth in tax revenues equivalent to its nominal GDP growth (Real GDP and Inflation). It is the smart measures that Revenue Authorities take which enhance funds mobilization to accelerate the economy. As per the IMF, around 15 percent tax to GDP growth, per annum, could ensure that the country has sufficient funds to invest in human capital/productive investments in the future, finance its liabilities and achieve the sustainable economic growth. Therefore, it is the consistent tax revenue growth that the FBR has to achieve that drives the overall growth of the economy.

It is about time that the agenda of tax reforms was implemented in its true spirit. The positive outcome of doing this will be unlocking tax revenue potential and fixing tax revenue-gap, which is intrinsic for Pakistan’s economic sustainability. Moreover, this can also help augment sustained public finances, broaden the tax base and accelerate GDP growth. Developing countries like Pakistan should have growth in tax revenues equivalent to its nominal GDP growth (Real GDP and Inflation). It is the smart measures that Revenue Authorities take which enhance funds mobilization to accelerate the economy. As per the IMF, around 15 percent tax to GDP growth, per annum, could ensure that the country has sufficient funds to invest in human capital/productive investments in the future, finance its liabilities and achieve the sustainable economic growth. Therefore, it is the consistent tax revenue growth that the FBR has to achieve that drives the overall growth of the economy.

It is worth mentioning here that the FBR has achieved its target for July-September 2020-21. The tax revenue collection by the FBR for July-September 2020-21 stood at Rs1,004 billion, indicating a growth of 4.69 percent versus Rs959 billion last year. In absolute terms, FBR’s tax revenue increased by Rs34 billion, which is 3.50 percent higher versus the target of Rs970 billion during July-September 2020. On average, FBR’s per month tax collection is around Rs335 billion during July-September 2020. It needs around Rs440 billion tax revenues during next nine months to accomplish the ambitious tax revenue target of Rs4,963 billion set for FY2020-21. With a projected GDP growth of 2.1 percent and CPI inflation 6.5 percent for FY2020-21, a realistic target for the FBR would be Rs4,341 billion. Additional measures require Rs622 billion for 2020-21. Anything above Rs.4,341 billion could be met though smart revenue measures or administrative steps taken by the FBR.

The Institute for Policy Reforms’ in a recent publication on “Pakistan debt and debt servicing Fact Sheet”, says; “We are in a debt trap that is entirely of our own making. It is a risk to our National Security.”

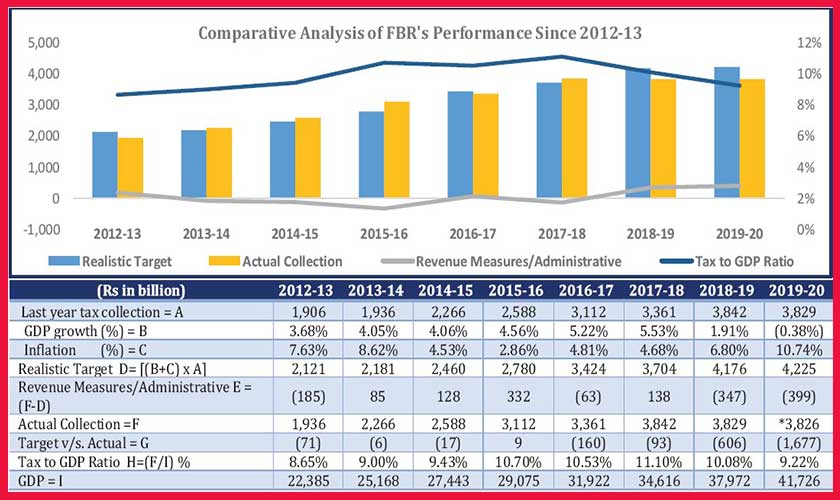

In pursuit of achieving tax revenue targets, the FBR chases the quantum impact of the GDP growth and inflation on the one hand, and revenue measures or administrative steps on the other hand. This reflects FBR’s performance. Hence, it is economic growth and the capacity of the FBR’s tax machinery which collectively attains tax revenue targets. The table depicts the actual performance of the FBR over the last eight years.

The present government, in agreement with IMF, projected a 44 percent growth in FBR’s tax revenues in 2019-20 despite an ongoing economic slowdown. This exaggerated growth was irrational and not based on ground realities. With a 0.38 percent negative GDP growth and 10.74 percent inflation, FBR’s realistic target was Rs4,225.68 billion in 2019-20. Whereas, IMF’s original target was Rs5,503 billion. Despite imposing additional and these hefty taxes worth Rs735 billion, the FBR failed in generating the required 44 percent growth in tax revenues. The growth of inflation could jack up tax revenue figures by Rs411 billion to Rs4,240 billion. However, failure in conducting reforms, recessionary effects of the economy and underperformance of the FBR collectively led to an increase in the tax shortfall up to Rs1,677 billion in 2019-20, which was unprecedented.

On top of it, the FBR failed to meet the inflation growth of 10.74 percent. This was a serious blow to FBR’s tax machinery. Consequently, FBR had collected actual tax revenue of Rs3,826 billion in 2019-20, which in absolute terms, was Rs3 billion lower than the tax revenues of last year. The tax-to-GDP ratio also dropped to 9.22 percent in 2019-20 as compared to 10.08 percent last year.

In 2018-19 the IMF’s original target was Rs4,435 billion. This target was later revised downwards twice from Rs4,435 billion to Rs4.398 billion and then to Rs4,150 billion due to an economic slowdown. With a 1.91 percent GDP growth and 6.80 percent inflation, the quantum impact of 8.71 percent growth had to be reflected in the tax revenue figures. In addition to this, out of Rs347 billion, FBR had taken around Rs200 billion tax revenue measures including imposition of regulatory duties. However, due to tight monetary and fiscal policies, it paralyzed the manufacturing sector, which negatively impacted GDP growth and revenue collection. FBR’s dismal performance can be gauged from the fact that neither smart revenue measures, nor quantum impact of economic growth, reflected in FBR’s tax revenue collection. Hence, after an exercise of the FBR’s tax machinery during one year, tax revenues remained stagnant at Rs3,829 billion in 2018-19 compared to Rs3.842 billion in 2017-18.

This even failed to match the inflation growth of 6.80 percent. The incremental tax revenue growth remained negative at Rs13 billion in 2018-19. This underperformance of the FBR led to the widening of the tax shortfall to Rs606 billion. Due to inefficiencies of the FBR management, unsustainable and unimaginable steps taken with revenue measures, the collection of the FBR nosedived. Hence, FBR’s accumulated tax shortfall has increased to Rs2,283 billion during the last two years. In effect, even after two years, FBR’ tax revenues are still lower than tax revenues Rs3,842 billion collected by it in 2017-18.

Pakistan had high GDP growth and low inflation during 2013-14 to 2017-18. This growth momentum reflected in FBR’s tax revenue collection. During 2013-14, with a GDP growth of 4.05 percent and 8.62 percent inflation, FBR’s realistic target was Rs2,181 billion. Whereas, FBR set the tax revenue target of Rs2,272 billion. With the combination of quantum impact of economic growth and revenue measures, FBR’s tax revenues increased by Rs330 billion from Rs1,936 billion in 2012-13 to Rs2,266 billion in 2013-14. It only registered a tax shortfall of Rs6 billion in 2013-14. Similarly, on account of smart tax revenue measures and quantum impact of economic growth during 2014-15, FBR’s tax revenues jumped to Rs2,588 billion compared to the target of Rs2,605 billion. The tax shortfall was a very nominal one, of Rs17 billion.

Fiscal Year 2015-16 was the only year in which the FBR surpassed its tax revenue collection targets and remained in surplus. It is the consistent growth in GDP which boosted tax revenue figures. With a high GDP growth of 4.56 percent and 2.86 percent inflation during 2015-16, FBR’s tax revenue collection grew by Rs524 billion to Rs3,112 billion as compared to Rs2,588 billion last year. The incremental revenues as a percentage of the tax revenue remained in double digits despite low inflation. The FBR’s shortfall was Rs160 billion during 2016-17 as FBR had set its tax revenue target of Rs3,521 billion which was Rs97 billion higher than realistic target of Rs3,424 billion. During 2017-18, with the ‘recipe’ of GDP growth of 5.53 percent and 4.68 percent inflation and FBR’s smart revenue measures, FBR’ tax revenue grew by Rs481 billion in one year. FBR’s tax revenues increased by a whopping 98 percent or Rs1,906 billion, from Rs1,936 billion in 2012-13 to Rs3,842 billion in 2017-18, which reflects a solid growth. In absolute terms, on an average, tax revenues grew by Rs381 billion during 2013-14 to 2017-18 versus the average tax shortfall of Rs1,141 billion during 2018-19 to 2019-20. On average, during 2013-14 to 2017-18, FBR tax revenues increased by around 1.0 percent of the GDP every year.

Prime Minister Imran Khan had a dream of raising FBR’s tax revenues to Rs8,000 billion and implementing tax reforms to boost Pakistan’s economy. However, it may be noted that the incumbent government has not even crossed the psychological barrier of Rs4 trillion as yet. Despite changing four FBR chairmen during the past 26 months, FBR’s accumulated negative collection stood at around Rs2.2 trillion. This was bridged through substantial borrowing and has ballooned public debt levels. In addition to this, process of tax reforms has still not been initiated. A stagnation in tax revenues increased fiscal deficits to alarming levels. This was the 2nd successive year in which the fiscal deficit remained over 8.0 percent of GDP. Almost 38 percent of GDP ie agriculture income and wholesale/retail trade, is not contributing significantly in the direct taxes. With such a huge parallel economy, we need to pursue reforms at a gradual pace, and give a vent to the businesses as well. Therefore, stagnation in the FBR’s tax revenue collection has put the country into a serious debt trap and has become a cause for concern for our national security, as rightly portrayed by the Institute for Policy Reforms.

If the federal government had implemented tax reforms, enhanced the tax net and saved these accumulated negative tax collections worth Rs2.3 trillion, around 60 percent of it could have been shared with the provinces for their socio-economic development. This 60 percent share amount stood at Rs1,369 billion. In addition to this, the rest 40 percent or Rs913 billion could have increased the country’s Defence Budget which is critical for regional security. The Security Budget of the State was Rs1,146 billion in 2018-19 and Rs1,213 billion in 2019-20.

According to the World Bank, Pakistan’s tax revenue potential is estimated around 26 percent of GDP, which implies a tax revenue gap of about 16 percent of GDP. As per the Finance Ministry, FBR’s tax revenue to GDP stands at 9.57 percent in 2019-20 which is amongst the lowest in the world. If the ‘status-quo’ is continued, raising tax collection of Rs8,000 billion by 2023 would be a distant dream.

The writer is a Fellow Chartered Accountant and Fellow Cost and Management Accountant and a member of Tax Reform Commission 2014