INSIGHT

Fiscal deficit - the mother of all economic ills - has alarmingly increased in the first quarter of 2016-17, which does not bode well for the remaining quarters. The stark figures released in the central bank’s latest economic report blatantly expose this vulnerability and couple it with collapsing exports. The report figures conjure up a bleak economic graph for the rest of the year.

The slightly unusual quarterly report of the State Bank of Pakistan (SBP), unlike previous reports, warns the government that drastic mid-course corrections and remedial measures would be required to achieve key macroeconomic targets. It implies in clear statistical terms that achievement of 3.8 percent fiscal deficit target set for 2016-17 would be a rather tall order.

The slightly unusual quarterly report of the State Bank of Pakistan (SBP), unlike previous reports, warns the government that drastic mid-course corrections and remedial measures would be required to achieve key macroeconomic targets. It implies in clear statistical terms that achievement of 3.8 percent fiscal deficit target set for 2016-17 would be a rather tall order.

The report released on December 30, 2016 has affirmed that most of the macroeconomic indicators are deteriorating as the first quarter experienced a widening fiscal deficit. Increased current account deficits further compound this issue.

The fiscal deficit soared to 1.3 percent of the GDP during July-September as compared to 1.1 percent of the corresponding period last year. Independent economists ominously forewarn that fiscal deficit could go as high as six percent of the GDP by June 30 this year, if timely action is not taken by the government.

This widening fiscal deficit peaked during the first quarter and has been the highest since 2011-12 even with an exceptional growth in the provincial surpluses and the comparatively smaller development funds released to the federal ministries and divisions.

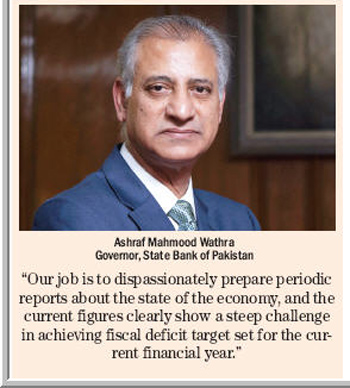

“Our job is to dispassionately prepare periodic reports about the state of the economy, and the current figures clearly show a steep challenge in achieving fiscal deficit target set for the current financial year,” Governor, State Bank of Pakistan (SBP) Ashraf Mahmood Wathra said.

He, however, seemed optimistic and predicted improvements in economic numbers, especially those related to fiscal deficit in the second quarter (September-December) hoping that the economic performance of the government would improve during the third and fourth quarters.

Wathra said the government was halfway through, and needed to bridge the already accumulative Rs150 billion fiscal deficit to improve economic performance at the end of 2016-17.

About falling exports, he said, he has been cautioning the government for the last three years to effectively deal with the issue. “But the good thing is that the government is about to offer the much needed relief package to the exporters,” he disclosed.

The central bank governor would not commit anything about the size of the package but informed that sources say it would be roughly $75 million and not $200 million as hinted by the commerce minister Khurram Dastgir Khan in the past.

He also hoped that the government would meet its $20 billion annual target for home remittances set for the current fiscal year and was of the view that the situation was not as dismal as was portrayed by certain quarters.

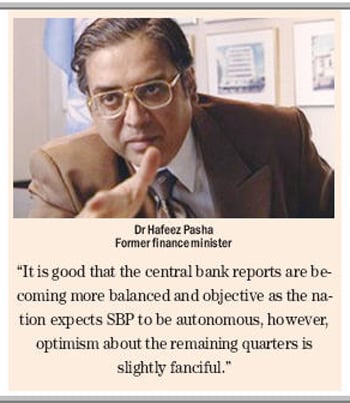

However, Wathra’s analysis did not find favour with renowned economist and former finance minister Dr Hafeez Pasha, who maintained that the second quarter would be worse than the first, as fiscal deficit and current account deficit numbers were very discouraging.

“It is good that the central bank reports are becoming more balanced and objective as the nation expects SBP to be autonomous, however, optimism about the remaining quarters is slightly fanciful,” Dr Pasha said.

The first two quarters, he said, witnessed 2.5 percent fiscal deficit (Rs750 billion), hence the achievement of 3.5 percent annual target would be a daunting challenge. “Our estimate is that fiscal deficit will eventually turn out to be in the range of five and six percent of the GDP,” he added.

He mentioned that the $900 million deficit in the current account was high due to a 20 percent increase in imports as well as the declining foreign direct investment (FDI). He also expressed concern over the burden on debt repayments, as net inflow of external borrowing goes negative. “There is hardly anything reassuring, as the government is borrowing extensively and it has borrowed over Rs1 trillion from the State Bank alone, which is deficit financing and detrimental to the economy.”

Independent economists and the government’s political opponents continue to disagree with the government and warn that future economic outlook gets murkier after the poor performance of the key macro- economic indicators in the first quarter.

The Pakistan Muslim League-Nawaz (PML-N) government like the previous Pakistan Peoples’ Party (PPP) and Pakistan Muslim League-Q (PML-Q) had enjoyed the financial comfort available through the Coalition Support Fund (CSF) and improved home remittances. That leverage is no longer available.

Former economic advisor to the Ministry of Finance Sakib Sherani also disagreed with the central bank governor and maintained that all major economic indicators were behind the set targets. “I am glad that the State Bank has finally spoken in its first quarterly report and the widening fiscal deficit showed the non-responsive attitude of the government.”

He did not see an improved outlook in 2017 for the Pakistani economy considering the current global economic environment as well as the geopolitical regional situation. “Under these circumstances weak fiscal position despite heavy borrowing from the central bank tells us that all is not well on the economic front,” he said, and added that July-September economic numbers were not very promising. “The government is borrowing at an unprecedented scale and after provincial transfers, there is a huge problem in debt servicing as revenues are falling and exports shrinking rapidly.”

Pakistan, he said, was headed towards a debt trap as the country was going back to the previous ten years position in terms of debt retirement after making provincial transfers and setting aside funds for the defence budget.

On the fiscal side, the government’s borrowing has reached record levels, which will eventually lead to

On the fiscal side, the government’s borrowing has reached record levels, which will eventually lead to  inflation and serious consequences down the road. Secondly, the returns on the national savings schemes, an unfunded debt, have come down as the government mobilised only Rs110 billion during the first quarter of the current financial year.

inflation and serious consequences down the road. Secondly, the returns on the national savings schemes, an unfunded debt, have come down as the government mobilised only Rs110 billion during the first quarter of the current financial year.

Unfortunately, there is no incentive to promote household savings through various saving schemes. Since borrowing through the central bank has no tangible consequences for the government, it continues to borrow, further increasing the debt burden.

The tax collection figures also followed the same dismal trajectory with just six to seven percent growth during the first six months. On top of that, the 17 percent tax collection target also seems too steep to be achieved by the tax authorities.

A former senior government official believes that revenue shortfall ranging between Rs300 to Rs350 billion will finally occur, which has already forced the Ministry Of Finance to cut the development budget. Ironically, while there was 25/30 percent cut applied on all development budget, special social development programme of MNAs amounting to Rs25 billion was completely exhausted to please the so-called legislators to help win them 2018 general election.

The revenue woes are due to the fact that there is no serious effort to reform the old dysfunctional and rigid tax structure. A cautious estimate says that the Federal Board of Revenue (FBR) annual tax target should be set at Rs6,500 billion (Rs6.5 trillion) to meet the growing expenditure against the current target of Rs3,500 billion (Rs3.5 trillion). Many believe that Rs8,000 billion (Rs8 trillion) revenue potential exists in the country. During one of the recent meetings, the chairman of the FBR had told the Senate Standing Committee on Finance that if income ordinance clause of 111(4) was removed, the government could double its tax revenue.

After revenues, the most worrying issue is decline in home remittances, as expatriates are preferring to send their money to Pakistan through the infamous ‘hundi’ and ‘hawala’ because of Rs4 difference between market and inter-market rate. Why is the central bank failing to manage this difference is difficult to fathom. This difference had not exceeded more than Rs1.5 during the last many years.

After revenues, the most worrying issue is decline in home remittances, as expatriates are preferring to send their money to Pakistan through the infamous ‘hundi’ and ‘hawala’ because of Rs4 difference between market and inter-market rate. Why is the central bank failing to manage this difference is difficult to fathom. This difference had not exceeded more than Rs1.5 during the last many years.

To say that market forces alone control the devaluation of our currency would be over-simplistic. A more sinister connivance at higher levels helps fix these rates that seriously hurt home remittances in particular and the whole economy in general.

If the current account deficit increased by 90 percent, FDI collapsed and went down by 48 percent, and the foreign exchange reserves witnessed a reduction of $750 million in the first two quarters, the targets set for the rest of the year seem impossibly difficult to achieve. The central bank report revealed that the current account deficit doubled to $1.381 billion from $579 million during the same period in 2015-16. The average CPI inflation rose to 3.9 percent on year on year (YOY) basis in the first quarter against 1.7 percent in the corresponding period of last year.

The good thing is that the central bank admitted that inflation rose because of swelling supply side factors, and the debt profile has further worsened. This means that the overall stock of public debt increased by Rs866.1 billion in the first quarter of the current financial year. External debt of the state sector rose by $1 billion to reach $58.8 billion by end-September 2016.

This external debt, according to independent economists, is $73 billion and not $58 billion as being claimed by the government. They allege that the public is being misled by manipulative figure work.

The positive thing is that the central bank report did not mince words and has warned the government to take notice of the current economic situation before it is too late. Large scale manufacturing growth is stagnating, private sector is still shy and borrowing less, and the overall economy seems to have gone off the government’s radar for now. The critical situation demands that rulers strive to salvage the economy which remains opaque for the commoners, instead of focusing only on overt political gimmickry.

The writer is a senior journalist based in Islamabad