FINANCE

Pakistan Muslim League-Nawaz (PML-N) government’s reckless domestic and external borrowing is scaling new peaks, as a result of which twin deficit (current account and fiscal) is getting out of control and may cause a serious balance of payments problems down the line.

The first four months of the fiscal year 2016-17 have witnessed a massive 60 percent increase in the current account deficit, which is anticipated to reach $7 billion by June 30 next year, compared to $2.5 billion last year. The most worrying thing, according to experts, is $3 billion worth of external borrowing in just four months.

The first four months of the fiscal year 2016-17 have witnessed a massive 60 percent increase in the current account deficit, which is anticipated to reach $7 billion by June 30 next year, compared to $2.5 billion last year. The most worrying thing, according to experts, is $3 billion worth of external borrowing in just four months.

Similarly fiscal deficit target of 3.8 percent of GDP, set for the current financial year, may jump to 5.5 percent of the GDP by June 30, 2017 as revenue growth in first five months remained 2 percent compared to 20 percent in the corresponding period last year.

The first quarter deficit was 1.3 percent of the GDP, which is more than 1/3 of the annual target because of the collapsing revenues of the Federal Board of Revenue (FBR).

In terms of rupee, fiscal deficit in the first four months of the current fiscal reached Rs450 billion and is feared to cross Rs2 trillion mark against the target of Rs1,250 billion by June 30 next year. From the central bank alone, the government has borrowed Rs1trillion during this period.

According to renowned economist and former finance minister Dr. Hafeez Ahmed Pasha, external borrowing in four months also includes $2 billion commercial loans through Skuk bonds and short-term borrowing from the commercial banks. Dr. Pasha questioned why the government needed to borrow in the presence of an import cover for four months.

The situation on the revenue side, he pointed out, is equally disturbing because of the low growth. The State Bank of Pakistan (SBP) in its first quarterly report, he said, conceded the government had borrowed Rs900 billion in three months. “Though they (government) have brought the inflation down but I really don’t know how they are going to justify this increasing domestic and external borrowing,” Dr Pasha said.

Generally, independent economists maintain that if there was no liquidity crunch because of the $23 billion foreign exchange reserves, now down at $19 billion, then why the ministry of finance and the SBP are seeking so much external borrowing. They also hold that out of a $2 billion worth of net borrowing, $1 billion went into debt repayment while another $1 billion was used to improve the current account balance.

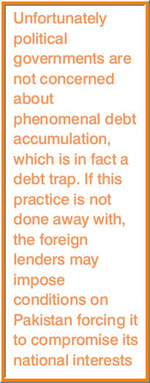

There is a growing consensus that external debt is rising because of the practice of financing current transactions, which is gravely shrinking debt repayment capacity. “Unfortunately political governments are not concerned about phenomenal debt accumulation, which is in fact a debt trap. If this practice is not done away with, the foreign lenders may impose conditions on Pakistan forcing it to compromise its national interests,” said an insider.

The fear of unknown besets even those official quarters, which maintain the buzzword is to ‘survive each financial year by getting local and foreign loans on day-to-day basis.’

The fear of unknown besets even those official quarters, which maintain the buzzword is to ‘survive each financial year by getting local and foreign loans on day-to-day basis.’

Over the years it has been proved that much of the external financing was sought not to develop new or complete current development projects but to meet existing debt repayment obligations.

That is why it is being said that sooner or later the government will have to go back to the IMF for new funding arrangements on the pattern of recently concluded three year $6.6 billion Extended Fund Facility (EFF) bailout package.

Economists and financial analysts argue that as long as the rate of return on borrowing is 1 percent higher than foreign debt, it does not create management problem. But in our case, it does not seem to be true as most of the new external loaning is aimed at managing annual budgets.

Efforts to boost reserves through better exports and encouraging more home remittances are nowhere on the government’s priority list as it’s only bent on securing foreign loans without realizing the consequences. Exports have fallen by 30 percent, and there is no likelihood the government would be able to meet its $20 billion home remittances target this year. Foreign exchange reserves that increased to a little over $23 billion have come down to $19 billion, forcing the government to seek more and more foreign loans to bolster them.

The failure in managing budgetary requirements is one of the reasons for borrowing from the central bank and commercial banks.

The high level of public debt with its large portion being financed through short-term instruments is no doubt a recipe for disaster. Furthermore, it challenges any country’s sovereign ability to meet its financial needs more sensibly according to the market conditions.

Since the government did not largely implement any homegrown or IMF-prescribed structural reform programme, one does not see any real cumulative impact of the macro-economic stabilization, particularly on the revenue and power sectors.

It happens because political considerations are not subordinate to economic considerations. A classic example is the recent unjustified massive increase in the salaries of the parliamentarians, a move that requires additional Rs400 million per annum. The pay-raise is said to be untenable especially when the government allocated only Rs170 million for human rights division, Rs218 million for crop insurance, and Rs150 million for the textile division in the current budget. Ironically, not a single word of objection was raised by the opposition against this two-fold increment in the salaries of the parliamentarians.

Then the very resolve of seeking documentation of the economy faced a terrible blow when the government was once again forced to extend yet another amnesty scheme to real estate sector, scuttling the FBR’s plan to collect additional Rs75 billion during the current financial year. How much new money could be whitened through the new amnesty scheme is yet not known but one thing is sure that this huge sector will go scot free without having to required taxes.

The FBR officials have reportedly opposed this new amnesty scheme but the political government thought it fit to support Qaisar Ahmad Sheikh, a businessman turned MNA who spearheaded the deal with the realty sector.

While increasing external debt and squeezing revenues are hemorrhaging the national kitty, the overall business environment remains unconducive to attracting local and foreign investment. The latest survey on Business Confidence Index (BCI), conducted by the Overseas Investors Chamber of Commerce and Industry (OICCI) during Sept-Oct 2016, revealed the business confidence had dropped by as much as 19 percentage points to only 17 percent compared to 36 percent in the last survey released in April this year.

Some of the key issues, the respondents expressed grave concerns over, are energy, price hike, security, law and order, government policies, regulations, dwindling exports, negative impact of new tax laws, and volatile political environment.

The decline in BCI was shared by all the sectors, showing manufacturing going down by 12 percent, and retail sector by 21 percent while services sector recorded a massive decline of 28 percent.

How can the government, which never misses an opportunity to trumpet about an economic turnaround, explain the falling exports and home remittances, ballooning external and domestic debt and other sectors’ underperformance? The government is often accused of over-stating the achievements yet to be realized to have come to pass to exogenous factors and ignoring weaknesses of the economy.

It does not take rocket science to understand that given the infrastructural bottlenecks and poor saving and investment rate, how the government would achieve 7 percent GDP growth rate in near future. With more and more people falling under the poverty line every passing day, unemployment remains far from contained. Notwithstanding, the official claim of alleviating the poverty from 55 percent to 39 percent, independent economists maintain the curse of poverty is rampant and the menace of unemployment is growing out of control because of the diminishing local and foreign investment.

If everything turns out alright, next elections will be held in 2018 and the important question is: What achievements will the government present before the nation? Removing load-shedding by generating 10,000 MW of electricity by 2017, perhaps this time, would not be sufficient enough to woo the voters.

The writer is a senior journalist based in Islamabad