INSIGHT

After giving a clean bill of health to the Pakistani economy in all its 12 reviews, the officials of the International Monetary Fund (IMF) have for the first time extensively talked about the rising external debt, declining foreign investment, collapsing exports, weakening revenue and failure in undertaking energy sector reforms.

The latest IMF report released at the conclusion of three year $6.65 billion bailout Extended Fund Facility (EFF) package reveals that all is not well on both the internal and external fronts.

The latest IMF report released at the conclusion of three year $6.65 billion bailout Extended Fund Facility (EFF) package reveals that all is not well on both the internal and external fronts.

The timing for the release of the report is being termed as very significant because the IMF‘s projections about the economy did not eventually come true, forcing its officials to change their stance on various issues.

External debt, now standing at $73 billion and feared to be reaching $90 billion in next two years, is one the serious issues that is fast becoming a major concern of every citizen. The pace with which the current government has been borrowing is reportedly causing problems to the officials of the ministry of finance and the central bank to manage debt related issues.

The matter compounded with the collapse of exports, leaving Pakistan behind even Bangladesh and Sri Lanka. External debt to export ratio has reached 300 percent compared to 120 percent of India and 100 percent of Bangladesh.

It is in that backdrop critics have started saying that Pakistan is fast entering into a debt trap, providing an opportunity to the International Financial Institutions (IFIs) to offer new loans on tough conditions.

The IMF, however, report avoided to offer some detailed account of rising unemployment and poverty and other social indicators across the county. There is 30 percent unemployment among the graduates. Today the government is providing 700,000 jobs annually compared to 1.4 million of 2013-14, which is worse than Bangladesh.

External debt amounting to $73 billion, according to them IMF should have been at $58.6 billion by June 2016.”Exports have been declining, private investment including Foreign Direct Investment (FDI) too low to support higher growth, public debt is still too high,” the IMF said in its report.

The obvious question being asked by the independent economists is how come IMF’s estimates went so wrong about the Pakistani economy and that why it did not raise these issues in all the 12 reviews. On the contrary, the Fund officials talked about the revival of the economy and stabilisation in all sectors. In September 2013, IMF estimated that exports would peak at $31 billion by June 2016 from $24.5 billion, which actually fell to just $20.8 billion by June 2016.

This shows that there had been a massive reduction of $10.2 billion in exports receipts during the last three years and would anybody ask the government where the much trumpeted economic turnaround is?

The ministries of finance and commerce have been holding responsible low international oil and commodities prices that caused reduction in exports. But other factors like unreal exchange rate and bad governance are not being mentioned for declining exports.

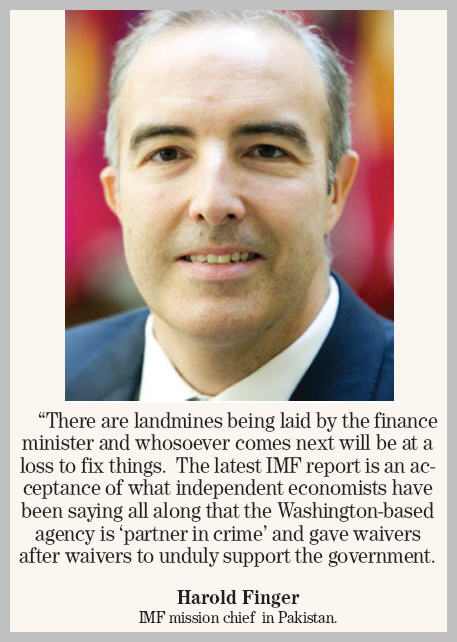

“We do see a decline in exports going forward due to appreciation of real effective exchange rate and governance challenges and power outage,” said Harold Finger, IMF mission chief in Pakistan. Regrettably, he used to sound very positive about the fast improving bigger economic indicators during his previous news conferences. What about his earlier claims that macro-economic situation has stabilised and that far less vulnerabilities are being faced by the government?

“We do see a decline in exports going forward due to appreciation of real effective exchange rate and governance challenges and power outage,” said Harold Finger, IMF mission chief in Pakistan. Regrettably, he used to sound very positive about the fast improving bigger economic indicators during his previous news conferences. What about his earlier claims that macro-economic situation has stabilised and that far less vulnerabilities are being faced by the government?

He and his other colleagues used to say every now and then that external buffers (reserves) have been strengthened, inflation is down, fiscal deficit is decreasing and structural reforms are on track. But in the new report, IMF has admitted that the situation on external debt, fiscal deficit, FDI, remittances and revenues is not satisfactory and needs attention of the government.

He and his other colleagues used to say every now and then that external buffers (reserves) have been strengthened, inflation is down, fiscal deficit is decreasing and structural reforms are on track. But in the new report, IMF has admitted that the situation on external debt, fiscal deficit, FDI, remittances and revenues is not satisfactory and needs attention of the government.

“There are landmines being laid by the finance minister and whosoever comes next will be at a loss to fix things,” said Ashfaque Hasan Khan, senior economist and Dean of Social Sciences at National University of Science and Technology (NUST).

He said the latest IMF report is an acceptance of what independent economists have been saying all along that the Washington-based agency is ‘partner in crime’ and gave waivers after waivers to unduly support the government.

One of the major questions being asked in the concerned quarters is that how the government would pulls through during the current financial year and beyond. The government is running its financial affairs by ruthlessly borrowing and so far acquired funds worth Rs1,682 billion which included Rs660 billion of the power sector, Rs622 billion of the commercial banks in connection with the commodity operation, withholding of Rs200 billion sales tax refunds of the exporters and by charging Rs260 billion advance tax. This all happened because of slow pace of reforms particularly in the energy and revenue sectors.

The IMF was originally set up to promote international economic cooperation and provide its member countries with short term loans to achieve balance of payments by trading with other countries. But now IMF is often accused of acting like a global loan shark, exerting huge leverage over the economies of more than 60 countries. These countries have to follow the IMF’s policies to get loans, international assistance and even debt relief.

More ironically now IMF decides how much debtor countries can spend on education, health care and environmental protection. It is generally believed that IMF is one of the most powerful institutions on earth.

According to former governor of central bank Dr Ishrat Hussain, road to prosperity needs sound macroeconomic and external sector management, energy sector restructuring, revamping of tax policy and administration, transfer of non-strategic assets, export sector revival and empowerment and strengthening of local governments.

He sees the successful completion of IMF’s three year EFF as a tool to stabilize the economy. However, he is very concerned about decline in exports, stagnation in home remittances, energy shortages and increase in circular debt, widening of current account deficit (up from $500million to $1.3billion in the first three months of the current financial year) and the ending of US Coalition Support Fund (CSF).

Moreover, the bleeding state sector enterprises have increased the government’s financial woes in many ways. On one hand there is a stalled privatisation program and on other hand these utilities are incurring huge losses. Accumulative losses of PIA, Steel Mills, Pakistan Railways and the power sector today stand at Rs 1.356 trillion and for the first time the IMF report acknowledged it by advising the government to take corrective measures to stop their growing annual losses.

Power sector remains the number one problem of the government as its losses both transmission and lines have come down just by five percentage point but they are far from being satisfactory. The losses of PIA, railways and steel mills along with power sector have turned out to be more than the

Power sector remains the number one problem of the government as its losses both transmission and lines have come down just by five percentage point but they are far from being satisfactory. The losses of PIA, railways and steel mills along with power sector have turned out to be more than the  annual development program of the country.

annual development program of the country.

Critics generally blamed the privatization ministry for inaction particularly on the part of its minister for not doing enough to sell the state sector entities. He is busy defending the government on television talk shows rather than looking after the highly subdued privatisation process in the country. So is the situation in Board of Investment (BoI) whose boss is also found indulging in political matters by regularly appearing in talk shows.

Major transactions including PIA, Steel mills, power utilities, railways, OGDCL and many others await privatisation. There is no doubt that international response for privatization is weak in most of the counties but then something is being done everywhere in terms of making the loss making public sector units into profitable ones and preparing them for their eventual disinvestment. But in Pakistan, the situation is totally different as the high ups of the privatisation are busy elsewhere to save their leaderships in the media.

Gone are the days when foreign investors used to visit Pakistan regularly and make investment both in the public and private sectors. FDI has come down to less than $900 million as against $5.5 billion of 2007-2008.

Gone are the days when foreign investors used to visit Pakistan regularly and make investment both in the public and private sectors. FDI has come down to less than $900 million as against $5.5 billion of 2007-2008.

Local investors are hesitant to make lot of investment because of the ever increasing political uncertainty and the government seems busy to tackle its survival problems and hardly finds time to address the issues of the investors and businessmen. The trading community, which has always been in favor of the PML(N) government , is much confused because of various issues including 0.3 percent withholding tax on all transactions. The increase in GST rate ranging from 16 to 50 percent is another irritant that is causing problems to the businessmen and exporters. The government could not offer any relief to the agitating business and trading community in this behalf.

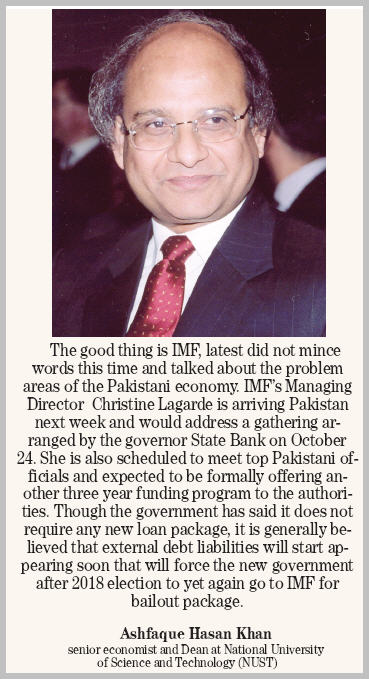

The good thing is IMF latest did not mince words this time and talked about the problem areas of the Pakistani economy. IMF’s Managing Director Christine Lagarde is arriving Pakistan next week and would address a gathering arranged by the Governor State Bank Ashraf Wathra on October 24.

The topic is: Emerging markets in the world economy”. She is also scheduled to meet top Pakistani officials and expected to be formally offering another three year funding program to the authorities. Though the government has said it does not require any new loan package, it is generally believed that external debt liabilities will start appearing soon that will force the new government after 2018 election to yet again go to IMF for bailout package. The loan alone taken by the PML (N) government during last three years is worth $14 billion, repayments of which by no means are an easy task for any succeeding government.

The writer is a senior journalist based in Islamabad