Print Story

X

The proposed measures include withdrawal of exemptions in sales tax and income tax; and reduced concessionary tax rates, besides growth in nominal GDP

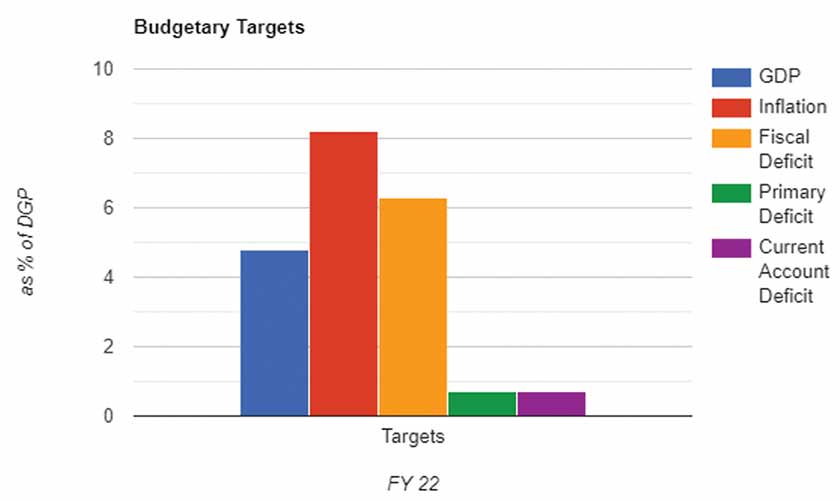

A provisional estimate of a GDP growth rate of 3.94 percent in the fiscal year 2021 (by the National Accounts Committee against the National Economic Council target of 2.1 percent) – and even lower projections of international finance institutions and the State Bank projection of 3 percent – has injected the policymakers with an unbounded enthusiasm. They have pitched the growth target for the next year at 4.8 percent and spun a macroeconomic framework that ought to be laid bare to maintain a sense of realism. In an environment where, in a first, the ruling party legislators are seen throwing budget documents at the opposition in the parliament, the future is hard to predict. Add the risk of an adverse development on the western border, rising world commodity prices and the ambiguity around the IMF programme, and the achievability of the growth target becomes that much harder.

Good intentions alone are not enough for a transition from stabilisation to growth. Extensive research undertaken at the Pakistan Institute of Development Economics (PIDE) has conclusively suggested that accelerated and sustained growth to absorb the country’s massive youth bulge and debt dependence requires a reset of the software. More than investment and consumption, the traditional drivers of growth that have landed the economy into a boom and bust cycle, growth requires root and branch reform of the stunted systems of policy, governance and regulation. Sadly, the official macroeconomic framework fails to reflect even a first step in this direction. Worse, inflation is targetted to decline to 8 percent from 9 percent. A push up has already been signalled by the recent raise in the prices of petroleum products.

Even in the traditional macroeconomic framework, growth in successful developing economies is driven by investment, especially private investment. In Pakistan, the targetted growth of 4.8 percent in FY22 is expected to come largely from consumption, (like FY21). In nominal terms, consumption grew by 16.1 percent in FY21 against 6.3 percent in FY20 when growth had become negative for the first time since the 1950s. The boost came from accelerated growth of workers’ remittances and rapid cash transfers under the Ehsaas Programme. At 13.9 percent, the growth rate of total investment was lower. Within this, despite the attractive Rs 2 trillion worth of credit incentives provided by the State Bank, the growth of private investment was only 6.6 percent. It had to be supplemented by a growth of 38.1 percent in public investment that itself had grown negatively over the previous two years. The pattern continues in FY22. Although a higher growth rate, 18.9 percent is projected for investment compared to 11.9 percent for consumption, it required a doubling of the growth rate of public investment (30.4 percent) compared to the private investment (15.3 percent). As a percentage of GDP, private investment is expected to increase by a mere 0.2 percentage points. What, then, is the point of the plethora of tax concessions being granted to the private sector?

As always in our economic experience, investment as a percentage of GDP exceeds the national saving rate by 0.7 percentage of GDP. In other words, the perennial deficit will resume after the aberration of a surplus in current account in FY21. There will be net borrowing from abroad of the order of Rs 377 billion. This is an under-projection as it presumes that the IMF will look the other way on the foot-dragging on some of the key conditionalities. Tax projections are also unrealistic, which raises the spectre of rising domestic debt. Tax collection rose by 18 perecent in FY21. The FBR target for the next year is to add more than a trillion rupees. The proposed measures include withdrawal of exemptions in sales tax and income tax; and reduced concessionary tax rates, besides growth in nominal GDP.

In an environment where, in a first, the ruling party legislators are seen throwing budget documents at the opposition in the parliament, the future is hard to predict.

The FBR collection is expected to increase from Rs 4.7 trillion to Rs 5.8 trillion, or by 23 percent as compared to the estimated collection in FY21. It is claimed that no new taxes have been levied and any additional revenue will be mobilised by expanding the base and through greater documentation. However, taxes increased and reduced/withdrawn seems to have an even division. For the purpose of the 7.5 percent withholding tax on non-filers, the Finance Bill has reduced the threshold of monthly electricity bill from Rs 75,000 to Rs 25,000. Sales tax on locally manufactured cars has been reduced from 17 percent to 12.5 percent. There will be no excise duty on 850cc cars. In addition, concessions will be given on electric cars. To make the environment business friendly and contain harassment, third-party audits and self-assessment have been introduced. Other measures include taxing profit on the debt component of pension funds. Many personal income tax exemptions stand withdrawn. Specified goods supplied in the border sustenance markets on the western border will enjoy exemption from sales tax. From 12.5 percent, withholding taxes on mobile phones are being reduced to 10 percent immediately and to 8 percent eventually. The rich will be made to pay according to their ability and the fixed income groups will be spared any additional burden. To incentivise the livestock sector, custom duty on vaccines and medicines is being removed. The paper used for the publication of Quran, auto-disable syringes and oxygen cylinders are now on the exemption list. Sugar has been put under the third schedule of Sales Tax Act to prevent arbitrary pricing.

According to a PIDE study, the federal government’s total debt and liabilities had reached a staggering Rs 37,078.5 billion by the end of April 2021, a nearly R 2,000 billion increase since June 2020. Out of the total budgeted expenditure of Rs 8,487 billion in FY22, 36 percent will go towards interest payments. A five percentage point proposal of decrease creates space for enhancing development expenditures. But the recent re-profiling into long term debt may not allow this. The Covid-related relief provided by G20 countries has also ended.

The federal government expects to raise over Rs 2.7 trillion from external resources, including Rs 2.69 trillion from external loans. This will increase the gross external resources in the upcoming fiscal year by over Rs 0.5 trillion. 55 percent of the external resources raised will, however, be used for repayment of foreign loans and credits. This represents a nine percentage point decrease in external resources share set aside for foreign loans and credit repayments. It is still higher than the share in FY21, when 40 percent of external resources were used for foreign loans and credit repayments. This was primarily due to rescheduling of debt payments following the coronavirus pandemic.

Pakistan’s debt and liabilities increased by nearly by Rs 2 trillion in the 10-month period from July 20-Apr 21. These are expected to further increase by the end of the current fiscal year on June 30. Despite increasing debt and liabilities, Pakistan’s debt servicing cost is on a downward trend. The final debt servicing cost for the upcoming year should further drop once the debt and liabilities figures for the entire FY21 are known. This represents a decreasing cost of debt despite an increase in debt, providing some relief. Public debt-GDP ratio is rather constant, but the debt service-revenue ratio is showing a downward trajectory. This, coupled with a slightly improving tax-GDP ratio and a falling debt servicing cost represent a good beginning to sustain debt levels over the coming years.

If the aim is not merely to sustain growth, but to also go for high levels of growth to provide opportunities for the new entrants in the labour force and manage debt, the PIDE’s Reform Agenda for Accelerated and Sustained Growth is the handbook to carry. It’s time the government consulted its own rather than be indebted in money as well as intellect.

The author is a senior economist, writer and speaker