Print Story

X

To enhance debt transparency, the government must prioritise creating a clear public debt management legal framework

| T |

he national economy has been severely impacted due to political instability. The country’s $3 billion standby arrangement with the International Monetary Fund is set to expire next month. Securing a new, significantly larger one, is among the top priority for the newly formed government.

An IMF team has arrived in Pakistan to meet with newly appointed finance minister, Mohammad Aurangzeb, and his team about the ongoing standby programme and a new loan programme. During the press briefing on March 7, Julie Kozak, the director of communications at the IMF, said that the focus is currently on completing the ongoing programme, which ends in April.

On the other hand, Pakistan is expected to request a new bailout package of $6 to $8 billion from the IMF to support its dwindling foreign exchange reserves and fulfil foreign payment commitments. It is still being determined whether the proposed bailout package can restore macroeconomic stability and boost investor confidence. Before delving into Pakistan’s external debt situation, let’s analyse the factors that have led to this challenging scenario.

Debt has been a part of human society since ancient times, and debt agreements have existed in various civilisations such as Mesopotamia, Egypt and Greece. Some of these agreements were vague and subject to interpretation by people in positions of power. In Medieval Europe, debt relationships were linked to social hierarchies due to feudal systems and serfdom.

The Renaissance era and beyond witnessed the evolution of modern banking and more complex debt instruments. However, widespread lack of transparency persisted, especially in dealings between private bankers and their clients.

Throughout the colonial era, European powers imposed debt on indigenous populations, often with exploitative terms.

The Industrial Revolution brought about significant changes in the global economy, such as the rise of big corporations and the expansion of financial markets. Debt instruments, such as bonds and stocks, have become more common, but the lack of transparency remains a concern. Financial markets proliferated in the 20thand 21st Centuries due to global capital flow and complex financial instruments.

However, this era also saw ‘debt opacity’ from off-balance sheet finance, complex derivatives and shadow banking. Debt opacity refers to a lack of clarity surrounding debt obligations, making it difficult for creditors and other stakeholders to understand the risks of lending or investing.

Legal scholars have developed another concept called ‘odious debt,’ which refers to debt taken on by a government that does not benefit the population and may even work against their interests. Over the past few decades, the idea of odious debt has been frequently brought up in different situations, particularly concerning developing nations governed by authoritarian or corrupt leaders.

Several countries, including Lebanon, Russia, Sri Lanka, Suriname and Zambia, have recently entered formal default; others, like Argentina, Ghana, Pakistan and El Salvador, also face debt issues. Pakistan’s external debt is increasing and concerns about transparency persist.

Several countries, including Lebanon, Russia, Sri Lanka, Suriname and Zambia, have recently reached formal default. Others, like Argentina, Ghana, Pakistan and El Salvador, too, face serious debt issues. Pakistan’s external debt is increasing and concerns about transparency persist.

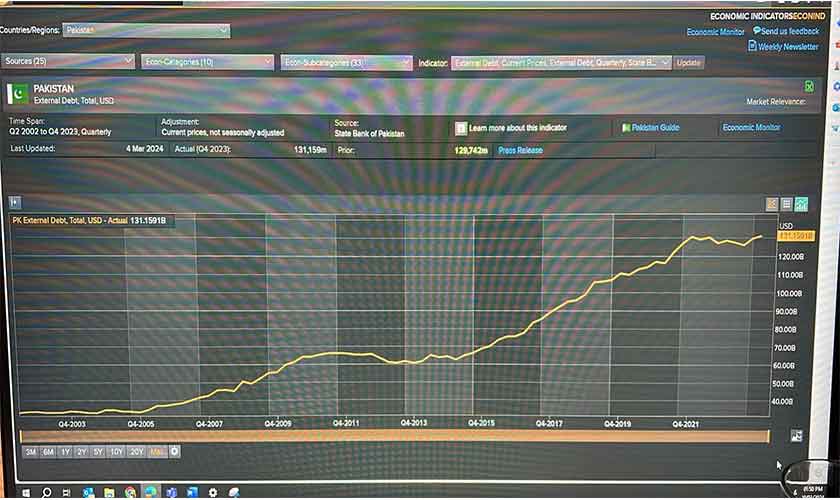

The external debt has risen sharply from $69 billion in 2015 to $131.15 billion in 2023. Pakistan’s current debt-to-GDP ratio is over 70 percent. Projections by the IMF and credit rating agencies suggest that a significant portion of the government’s revenues will go towards interest payments on its debt this year. Approximately 85 percent of Pakistan’s external debt stock is in dollars and is owed to bilateral and multilateral creditors.

External debt 2002–23

In addition, a recent report published by Tabadlab, a think tank, states that each citizen now has a debt of Rs 321,341 or $1,150.58. This highlights the severity of Pakistan’s deteriorating debt, which is worse than many people realise. The situation could lead to a default on payments and cause a significant economic downturn.

Pakistan has met the targets set by the IMF for the second review and is on track to receive the $1.1 billion final tranche under the SBA programme. Nevertheless, securing the new loan programme before the next budget would be a significant challenge for the government.

Prime Minister Shahbaz Sharif has split the Ministry of Finance, Revenue and Economic Affairs into separate entities. Muhammad Aurangzeb, a senior banker, has been appointed to run the finance and revenue affairs. As economic affairs minister, Ahad Cheema has been asked to handle external debt.

This decision may have unforeseen consequences. The question is how new borrowings will be used for the benefit of the people. Concerns have been raised that public debt has been accumulating without transparency and accountability.

It is essential to ensure responsible debt management in the interest of the country’s citizens. Besides paying back foreign loans with interest, the debt has financed development projects of which some have not been universally popular. This has led to the argument that some of the debt is ‘odious.’

Pakistan is also struggling to resolve its energy sector issues. Energy sector losses remain high and the circular debt is now around Rs 5.7 trillion for the gas and power sectors.

To enhance debt transparency, the government must prioritise creating a clear public debt management legal framework. It should mandate disclosure of public debt information, regulate its content and frequency, and ensure easy access for stakeholders. It is important to release core public and publicly guaranteed debt data yearly. The government should also develop rigorous analytical and monitoring processes for approving and implementing resource-backed loans.

The writer is a senior lecturer in finance and heads the business finance programme at Birmingham City University, UK. His X handle is @HafizUsmanRana